{kind=link}

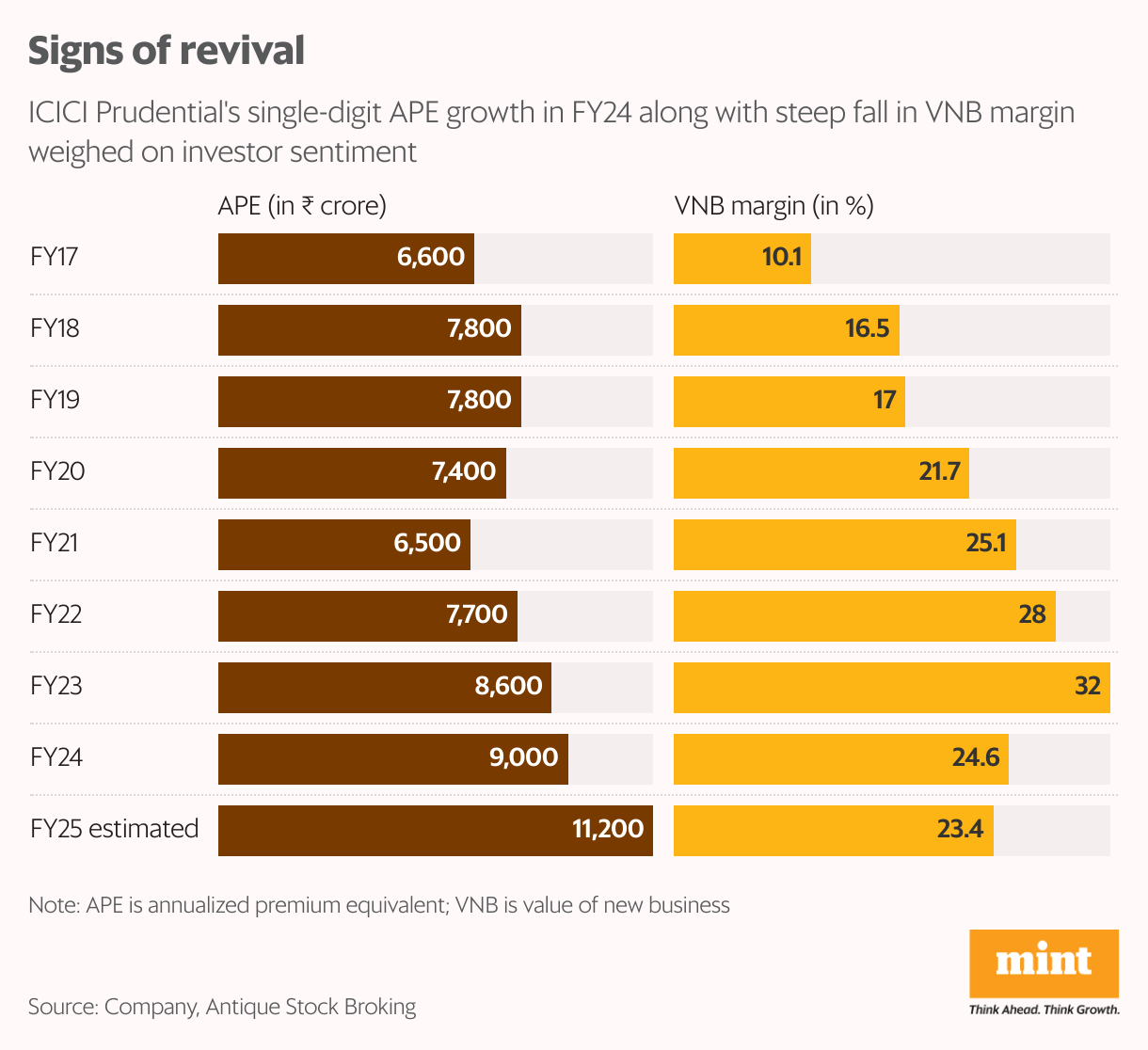

In July, ICICI Prudential Life Insurance Co. Ltd shares finally crossed their previous all-time high of ₹724.30 seen almost three years ago on 8 September 2021. Despite the growth in embedded value at a compound annual growth rate (CAGR) of about 16% over the last two years to FY24, the company’s shares have faced valuation de-rating. Its price to embedded value multiple came down to 2.2x based on FY25 brokerages’ estimates from close to 3.2x for FY22.

Embedded value or the modified form of book value is a total of adjusted book value, and the present value of the future profit locked in existing policies.

The valuation de-rating can be attributed to the disappointment over the trend in two important financial parameters. Annualized premium equivalent (APE) or total revenue for the company grew by just 4.7% year-on-year in FY24. To add to the woes, economic profit margin, also known as the value of new business (VNB) margin fell to 24.6% in FY24 from 32% a year ago, as the share of ULIP, a less profitable product, rose in overall APE to 43% from 36%.

The renewed interest in the ICICI Prudential stock is mainly owing to the faster APE growth of 34.4% in the June quarter (Q1FY25), which has rekindled hopes of investors. Growth was led primarily by a 78% jump in ULIP sales that now accounts for 51% of APE. Though it has dragged the VNB margin by 600 basis points year-on-year to 24%, similar to last financial year’s margin, indicating that further downside to the margin could be limited.

During the interaction with analysts last week, the company’s management reiterated the industry demand for adoption of accounting based on International Financial Reporting Standards (IFRS). The accounting in insurance as per Indian accounting standards, especially in life insurance, is such that it depresses the reported profit and earnings per share. Consequently, the price-to-earnings ratio for companies such as ICICI Prudential looks rather high at above 100x for FY25 estimated earnings of some brokerages.

For example, Indian accounting standards require recognition of entire customer acquisition cost such as commission paid to agents to be recognized upfront in the profit and loss account whereas IFRS 17 allows for the deferment of such costs. Along with the adoption of IFRS, there is also the demand for risk-based capital requirement instead of solvency based. The risk-based requirement allows for differential capital requirements based on the size and risk involved in the operations of an insurance company, instead of uniform solvency-based capital for all companies. The company’s management believes that, if the new capital parameter is introduced, it would mean lower capital requirement and aid higher growth.

Going forward, VNB growth should mirror APE growth as the bulk of the cost increase seems to be behind and operating leverage is expected to kick in. VNB growth would largely be a function of product mix. Hence, the endeavor would be to improve product level margins by extending the tenure, increasing sum assured, providing higher attachment/ riders, etc. The company remains focused on absolute VNB growth with no specific target margin. It has been walking away from businesses with negative/low margins.

As such, there could be further upgrades to analysts’ estimates based on ICICI Prudential’s strong 28.5% year-on-year APE growth in the first five months of FY25. Analysts from Emkay Global Financial Services note there is an upside risk to their FY25 APE estimate. They also add that there is relatively lower risk to the company from the new surrender regulations that are applicable from October as it has lower dependence on non-linked saving products at 17% of APE for Q1FY25.