{kind=link}

The seasonally adjusted HSBC India Manufacturing Purchasing Managers’ Index (PMI) fell to an eight-month low of 56.5 in September from 57.5 in August. A reading of 50 separates expansion from contraction. With manufacturing growth softening throughout the September quarter, the average PMI reading slipped to its lowest since the December quarter, said the PMI survey report.

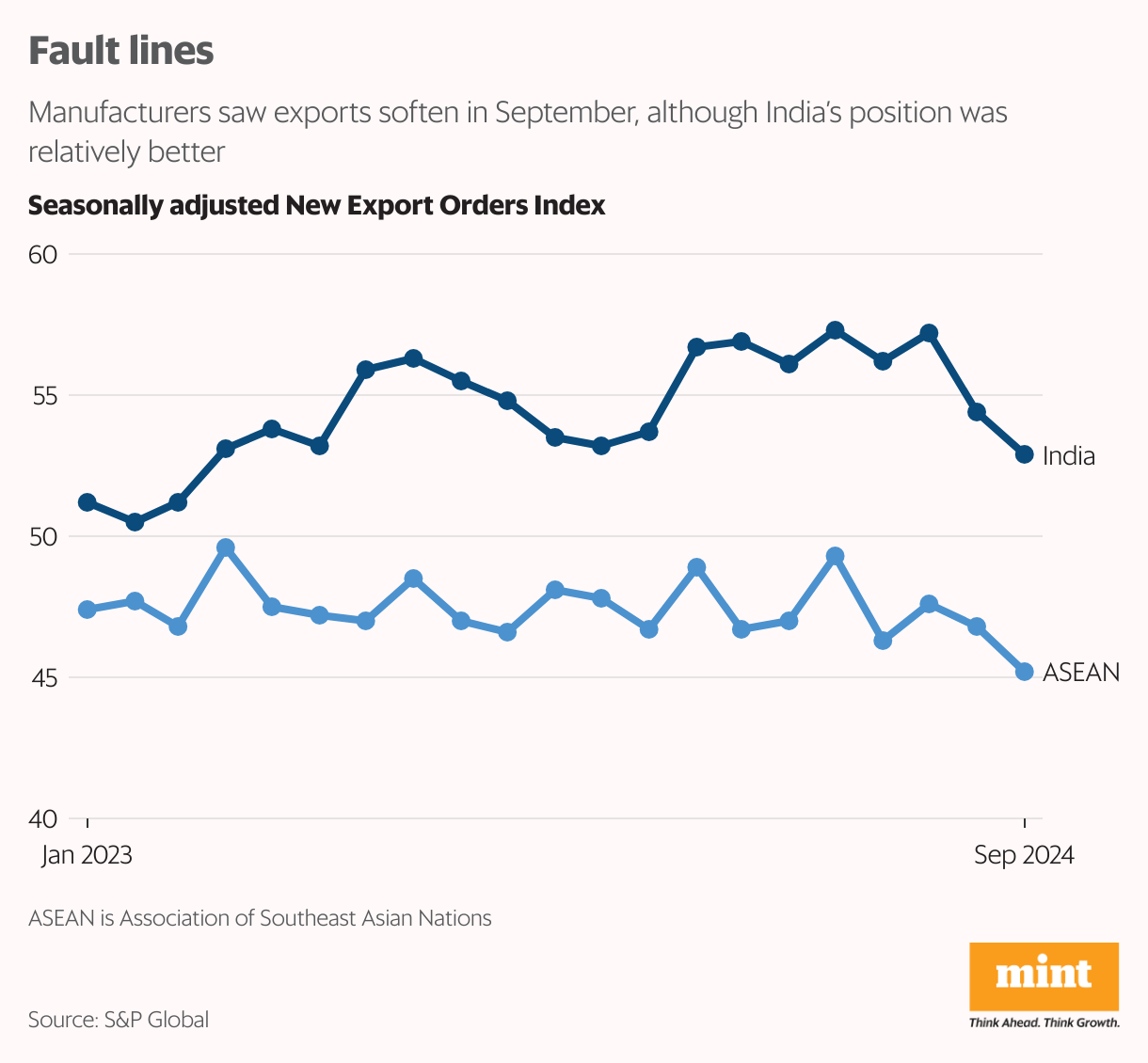

The pain points: Rates of expansion in factory production and sales receded for the third straight month in September. Plus, international orders or exports rose at the slowest pace in a year-and-a half. After a lukewarm September quarter, domestic manufacturing demand is expected to get a push from the upcoming festival season. However, no cheer is anticipated on exports amid muted global growth and geopolitical challenges.

Asian exports could shift down a gear over the coming months, Nomura Global Markets Research said in a report dated 30 September. Nomura’s leading index of Asian exports fell to 99.5 in October from 103.1 in September, registering the largest drop in 23 months. This index comprises nine components and has a three-month lead time.

The sharp fall was driven by weakness in China’s imports and emerging market PMIs. “This is in line with Germany being on the verge of a recession, still-weak China demand and the US manufacturing ISM being in contractionary territory,” Nomura added. Sure, China’s recent bazooka stimulus may eventually stoke demand, but the results will take time.

The problem of subdued exports is not unique to India. The New Export Orders index for the ASEAN pack remained in the contraction zone at 45.2 in September. In comparison, the reading for India, although lower than in August, was in the expansion zone at 52.9. But a prolonged weakness in goods exports could be an impediment to India’s growth story, which is considered to be better placed on the macro-economic front than many Asian peers.

In August, India’s trade deficit widened to a 10-month high adversely hurt by falling merchandise exports and record high imports. The trade deficit is set to widen further. This is largely due to weakness in goods exports, which is likely to continue as Indian manufacturers struggle to compete against their Chinese counterparts, pointed out a recent Capital Economics report.

Merchandise export growth over April to August in FY25 is muted at 1.1% after declining in the same period last year. “We expect merchandise export growth to remain on the softer side with growth slowdown in the developed markets,” said Gaura Sen Gupta, economist at IDFC First Bank. Thus, India’s FY25 GDP growth is expected to be supported by domestic demand and a likely revival in rural demand. “The drag from net imports is expected to rise in FY25, with domestic demand remaining relatively stronger than external demand,” she added.

Meanwhile, the PMI survey showed that input cost pressures rose in September, with panellists citing increased chemical, packaging, plastic and metal prices. This, along with higher labour costs, prompted manufacturers to raise selling prices. That said, the price hikes were moderate and were similar to those seen for input costs.

For now, around 23% of Indian manufacturers forecast output growth in the year ahead, while the remaining firms predict no change. Hence, the overall level of business confidence measured via the Future Output Index fell to its lowest since April 2023.