{kind=link}

MUMBAI

:

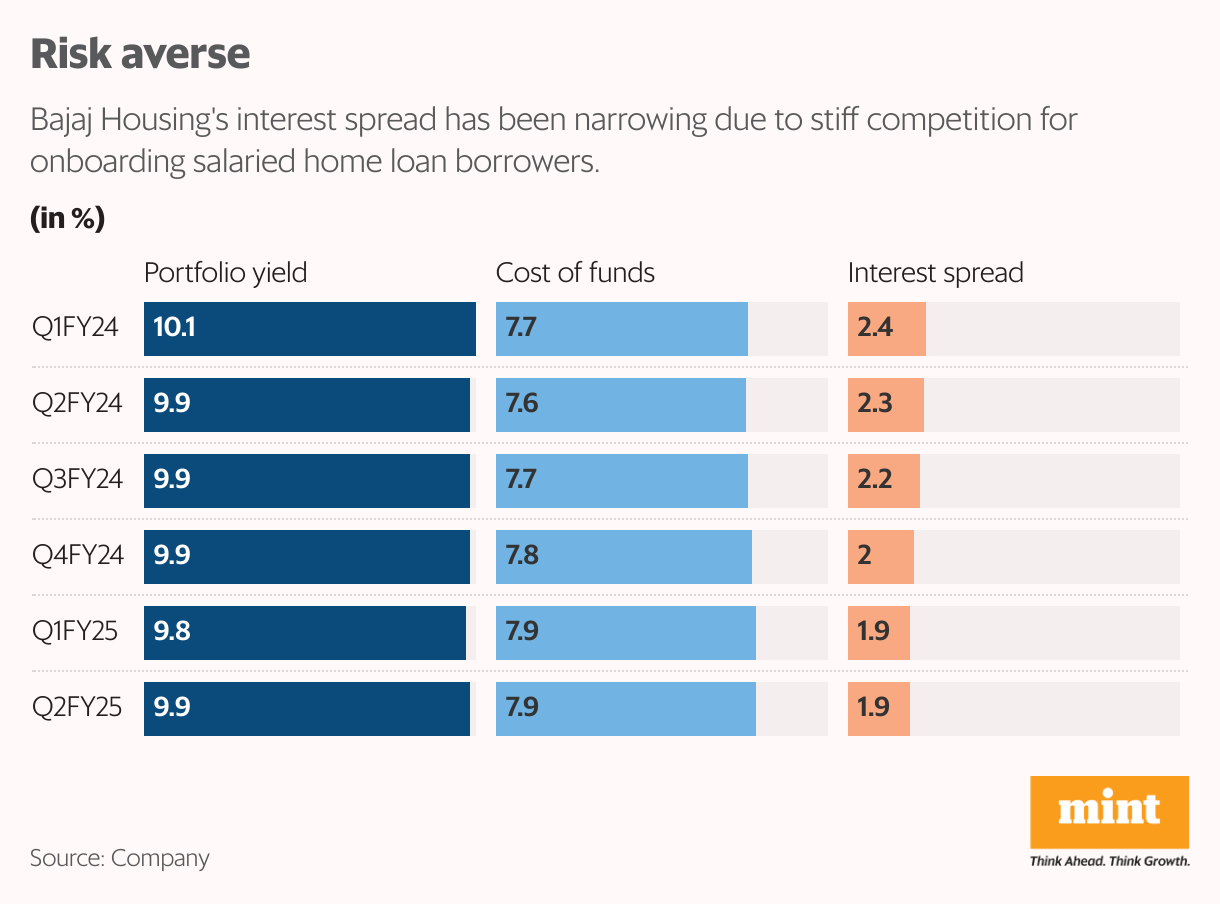

Bajaj Housing Finance Ltd has come out with first quarterly results post listing after separation from Bajaj Finance Ltd. After its bumper listing, the stock’s performance has been muted. This could indicate investors’ concern about interest spread or the gap between yield on advances and the cost of borrowings at 1.9% in the September quarter (Q2FY25) versus 2.3% a year ago.

Lower interest spreads lead to lower return ratios. Sure, Bajaj Housing has a lower spread, and the business model has less risk by virtue of being a mortgage lender. However, its return on assets (RoA) at 2.5% for Q2FY25 is much lower than parent Bajaj Finance’s RoA of 5% plus seen in Q1FY25.

Generally, a higher RoA business also means a higher return on equity (RoE), culminating in a higher valuation. Bajaj Finance standalone is quoting at a price-to-earnings (P/E) multiple of 25x, while Bajaj Housing is at 50x based on Bloomberg consensus estimates for FY25. On a price-to-book (P/B), too, the former is at 4.6x and the latter at 5.7x based on FY25 estimates, according to Bloomberg.

The valuation conundrum

Against this backdrop, the moot question is whether Bajaj Housing should quote at a premium to Bajaj Finance. The premium becomes glaring if Bajaj Finance’s market capitalization is adjusted for its 89% holding value in Bajaj Housing, even after factoring in a holding company discount of 25%. Notably, HDFC Bank, the biggest private sector lender with a substantial mortgage book after the merger with HDFC, is quoting at a price-to-book value of 2.25x (excluding the value of subsidiaries) based on FY25 estimates. This either means that Bajaj Finance and HDFC Bank are undervalued or Bajaj Housing is overvalued.

In Q2, net interest income (NII) grew by only 13% year-on-year (y-o-y)to ₹2,227 crore despite the loan book growth of 27% to ₹89,878 crore. The lower growth rate in NII versus loan book reflects the pressure on interest spread. The only solace is that the spread has been stable sequentially at 1.9%, indicating it might have bottomed out for now. Other income surged 43% y-o-y to ₹184 crore, driven by sharp growth in income from derecognized loans. The cost-to-income ratio dropped. Profit after tax rose by 21% to ₹546 crore.

While Bajaj Housing appears like a decent bet on the salaried home loan segment having benign credit costs, it would not be a bad idea to keep a tab on the valuation of Bajaj Finance, the parent company, and HDFC Bank.