{kind=link}

Agrochemicals company PI Industries Ltd is facing headwinds as its key customer, Kumiai Chemical, reported modest revenue growth for the quarter ending July and indicated a weaker October quarter. Kumiai accounts for over half of PI’s total sales and thus has a big influence on its performance.

Another worry is the potential further market disruption caused by the patent expiry for its key product, pyroxasulfone, and the expected entry of a Chinese company that has received approval to manufacture it. However, the immediate impact may be limited, as the product is largely sold on a cost-plus basis.

Pyroxasulfone, a herbicide used to control grasses and weeds, accounts for 35-40% of PI’s revenue. It is manufactured exclusively for Kumiai.

Kumiai has projected a drop in its Axeev sales, the product based on pyroxasulfone, for FY24 due to de-stocking and weakness in global agri-input market. Kumiai’s financial year ends in October. It has also announced a change in top management.

“Whether the management transition leads to any change in ordering patterns by Kumiai from PI remains to be seen,” said a report by Kotak Institutional Equities on 6 September.

PI has been investing in new product development and acquisitions in related areas to expand its product portfolio. It commercialised four new products in the June quarter (Q1FY25) and is likely to commercialise five more products in FY25.

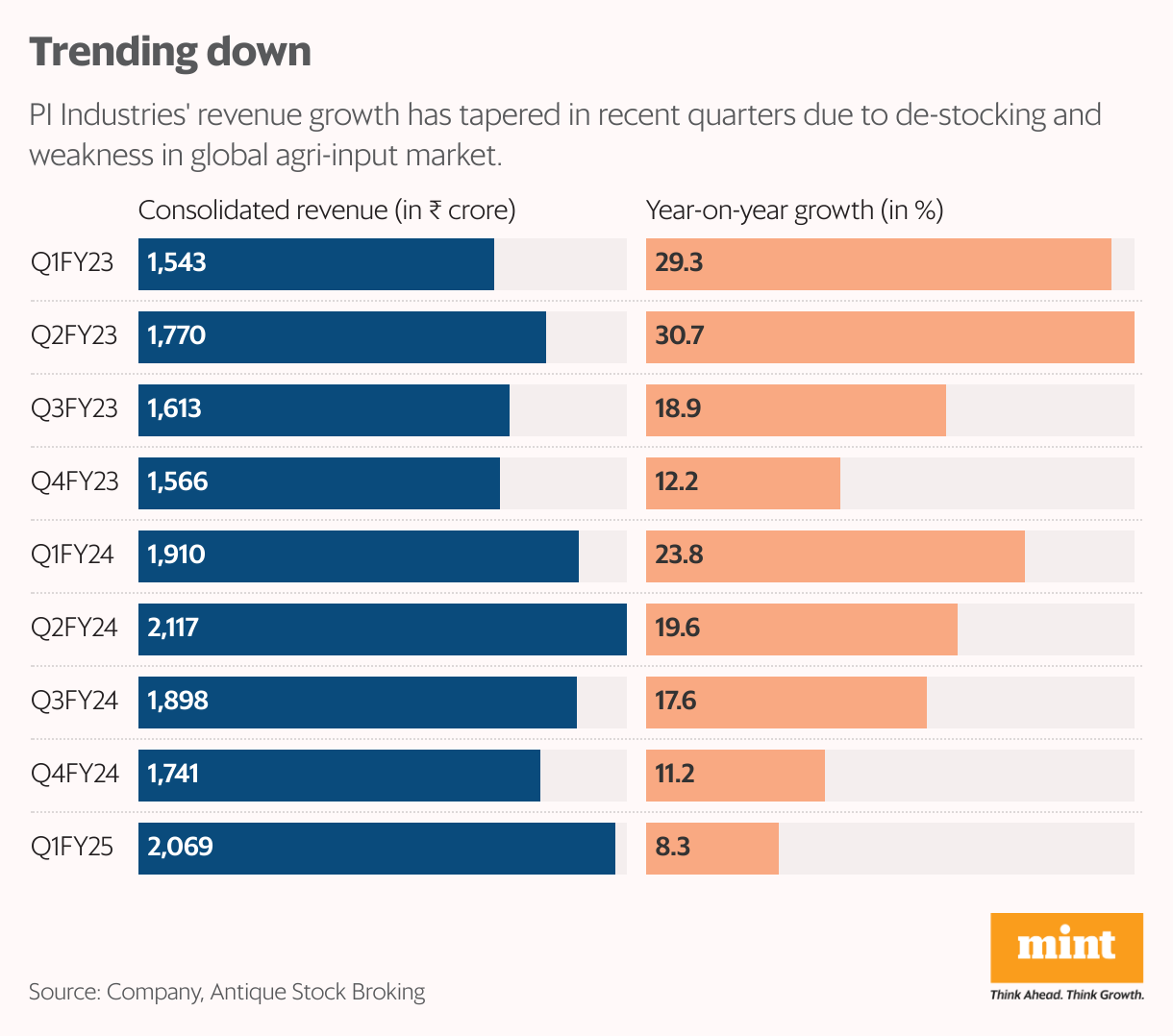

Revenue from new products was up 24% year-on-year last quarter versus the aggregate growth of 8%. Still, improving product mix along with operating leverage meant PI’s Ebitda increased by 25% last quarter. According to the management, the share of new products is projected to increase from about 20% in its custom synthesis manufacturing business to 30-35%.

Also Read: Heavy showers could rain on agrochemical firms’ parade in Q2

Meanwhile, PI has made an offer to acquire Plant Health Care (PHC) plc, a UK-based company in the crop protection business, for £32.8 million (about ₹360 crore). However, PHC’s current contribution to revenue would be a mere 1.3%. PI’s management stated in the latest earnings call that it is actively evaluating other inorganic opportunities, supported by a cash balance of almost ₹4,000 crore.

However, its diversification strategy is yet to show results. “Though we believe the company is taking efforts for diversification in pharma, electronic segments, as well as ex-pyroxa agri-chem portfolio, particularly biological products; we await meaningful contribution from the same,” said JM Financial Institutional Securities Ltd after the Q1FY25 results.

Amid uncertainties on business prospects, PI’s shares have gained around 26% in the past one year, lagging the Nifty 500’s 34% rise. The stock trades at a price-to-earnings multiple of 41.5x based on FY25 estimates. How the market dynamics evolve for its key product would be crucial ahead.

Also Read: Chemicals companies’ capex intensity is poised to take a breather