{kind=link}

The primary objective of the fresh issue is to strengthen the capital base, which is essential for maintaining and enhancing its solvency levels.

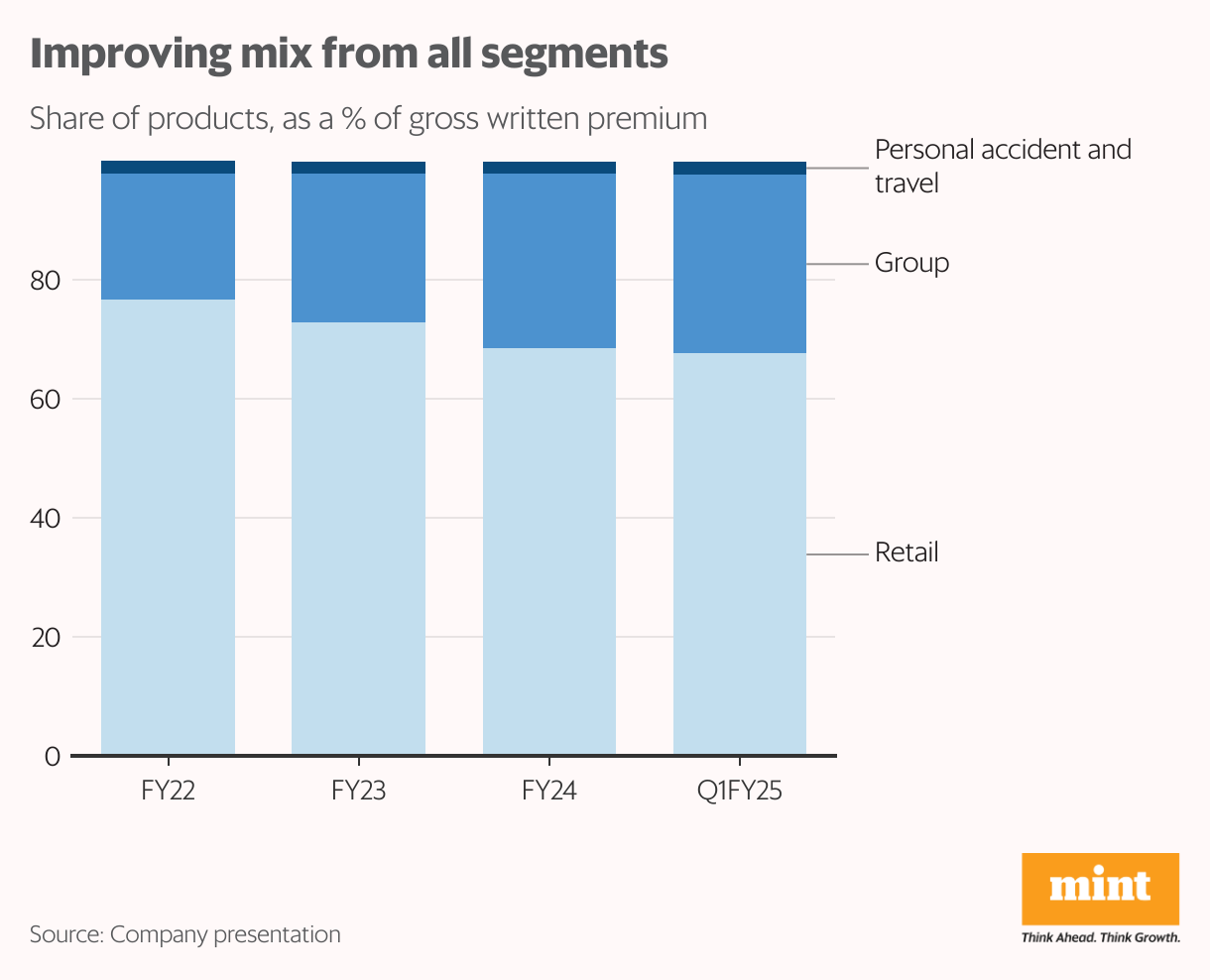

Niva is among India’s largest and fastest-growing insurers in the industry. The company focuses on the retail health insurance market, which currently accounts for about two-thirds of its gross written premium (GWP). As this segment of retail health insurance continues to grow, Niva Bupa is well-positioned to take advantage of the increasing demand for health insurance products. However, it also faces strong competition from other insurers and ongoing challenges in achieving profitability.

Also read | Swiggy IPO: Navigating a competitive landscape. Can it deliver?

Balanced revenues

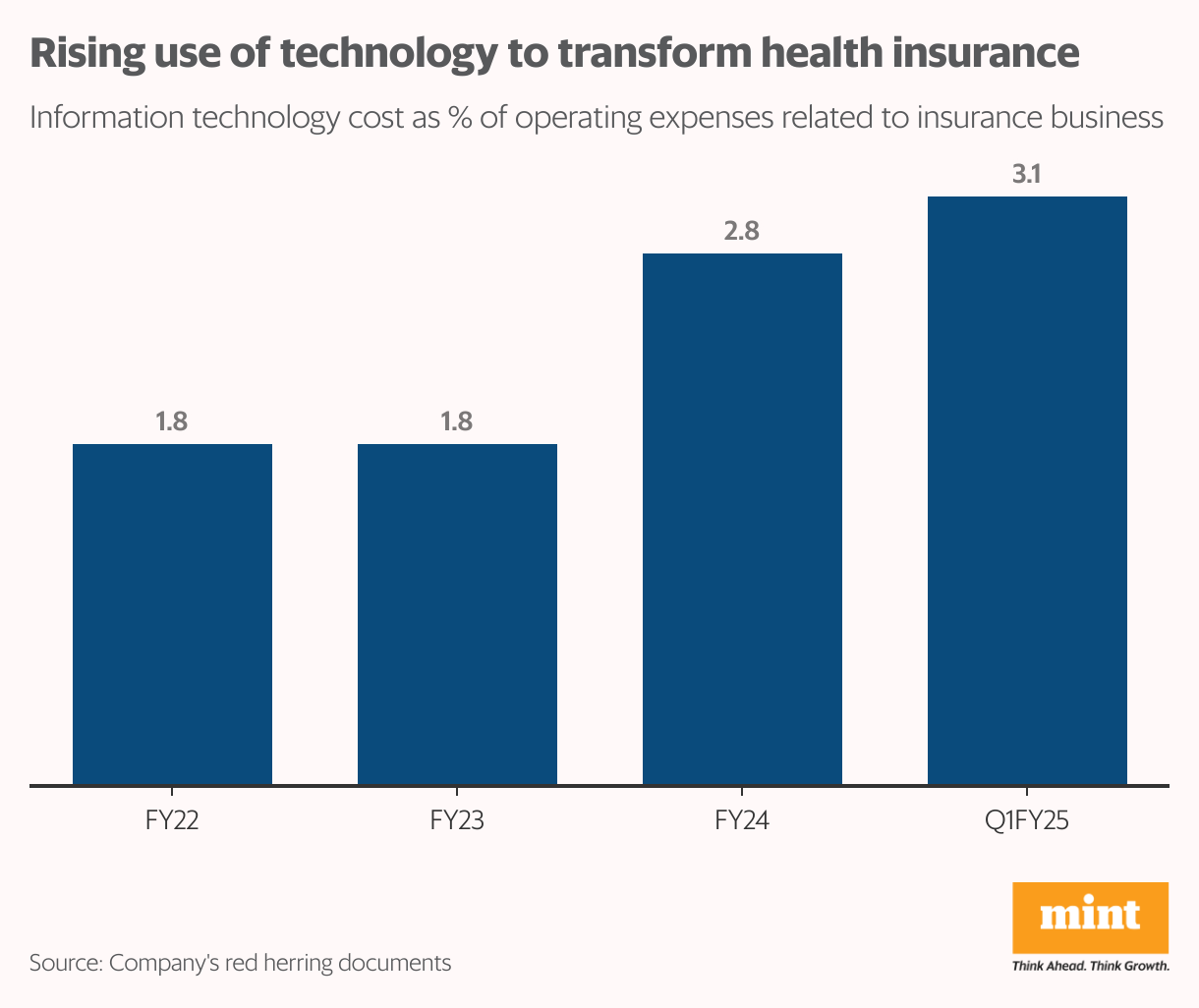

Niva has demonstrated a resilient and diverse revenue stream, driven by rising technological spends that streamline operations and improve customer experiences. Over the past three years, the company’s gross written premium has grown at a compound annual growth rate (CAGR) of 41.3%. Its retail segment, which remains the primary contributor, reported an average growth rate of over 72% between FY21 and FY24, reinforcing the company’s robust market position. Additionally, the group business segment experienced an average growth rate of over 25% during the same period, contributing to the overall upward trajectory.

The company’s commitment to technology is evident in the substantial increase in information technology spending as a percentage of operating expenses. “Over 50% of our new policies are processed digitally without any human intervention, and a substantial portion of our cashless claims are now auto-adjudicated. This end-to-end digital transformation from digital claim forms to automated medical rule applications has been instrumental in reducing operational costs,” said Vishwanath Mahendra, chief financial officer at Niva Bupa, in an interview with Mint.

It stands out with a wide range of products designed to cater to diverse customer needs, complemented by a technology-driven, automated approach to customer service. Renowned for its strong presence in health insurance and healthcare, the company also boasts deep expertise in claims and provider management, as noted in a research report by Bajaj Broking.

Profitability pressure

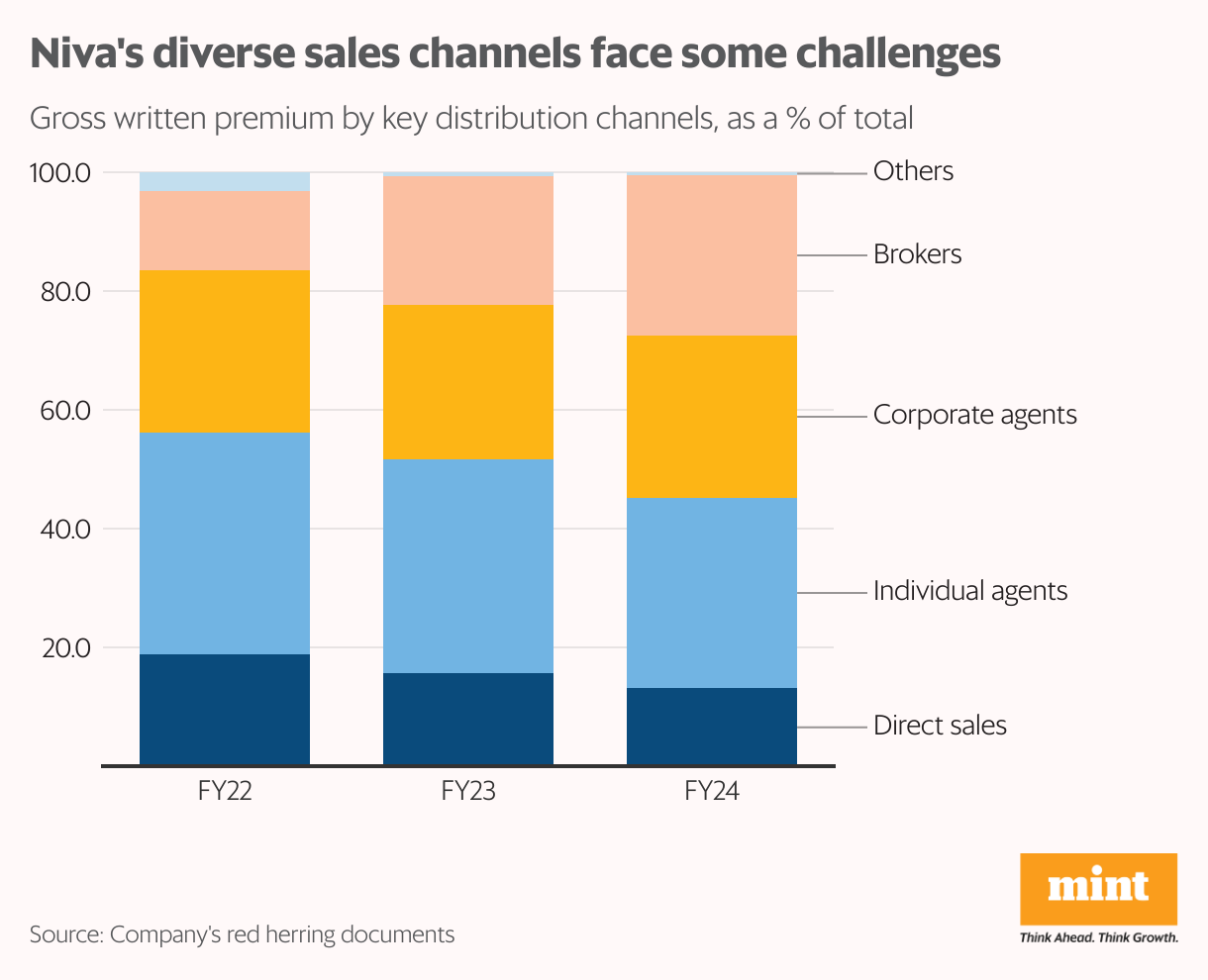

Niva Bupa’s diverse sales channels provide extensive market reach, but also present challenges in maintaining consistent performance. Additionally, the company’s growth ambitions could be tempered by ongoing profitability pressures. In recent years, it has strategically shifted towards indirect sales channels, with a notable increase in broker contributions.

Meanwhile, direct sales have seen a slight decline, from 18.8% in FY22 to 13.1% in FY24. “Actually, our direct and agent sales are not in decline; rather, they’re infact growing steadily,” Mahendra said. “However, since our other channels such as digital and broker sales are expanding at a faster rate, it may create an impression of a slower growth rate in direct and agent channels. It’s important to consider our growth relative to the overall market,” he added.

Also read: Afcons IPO: Your ticket to India’s infrastructure boom?

Analysts also feel that to drive business growth and capture a larger market share, Niva Bupa should focus on strengthening its distribution network, which is crucial for expanding its reach. “Strategic tie-ups with large insurance partners, as well as leveraging bancassurance models, will play a key role in this expansion. Enhancing relationships with agents and broadening the distribution network will help tap into new customer segments. By increasing the accessibility of its products and services, Niva Bupa can significantly boost its business prospects and further solidify its position in the market,” said Kranthi Bathini, director of equity strategy at Mumbai-based WealthMills Securities.

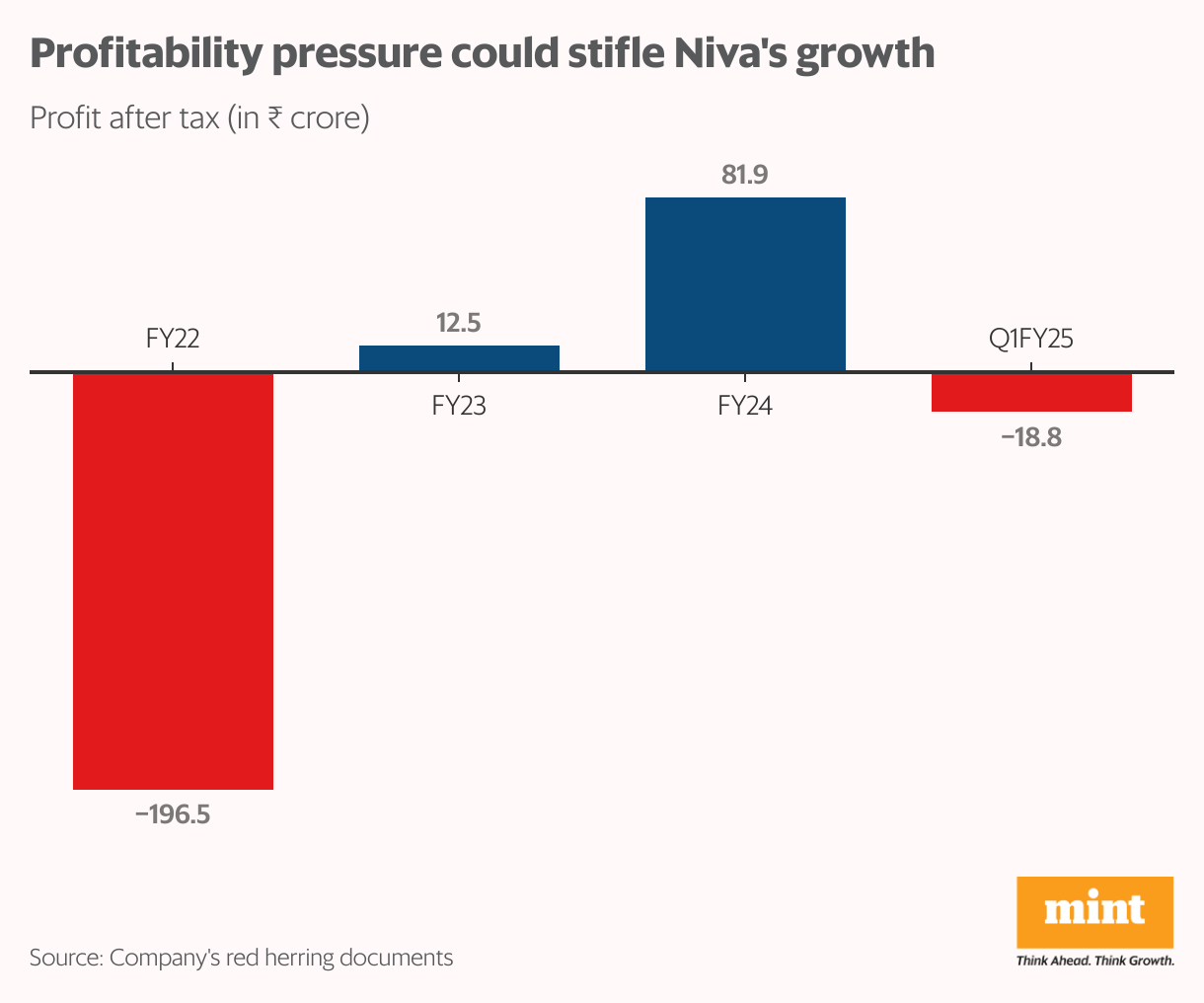

The insurer’s profitability has been under pressure in recent years. The company reported a significant loss of ₹196.5 crore in FY22, followed by a marginal profit of ₹12.5 crore in FY23. While FY24 witnessed a recovery with a profit of ₹81.9 crore, the recent quarter, Q1 FY25, saw a setback with a loss of ₹18.8 crore.

Stiff competition

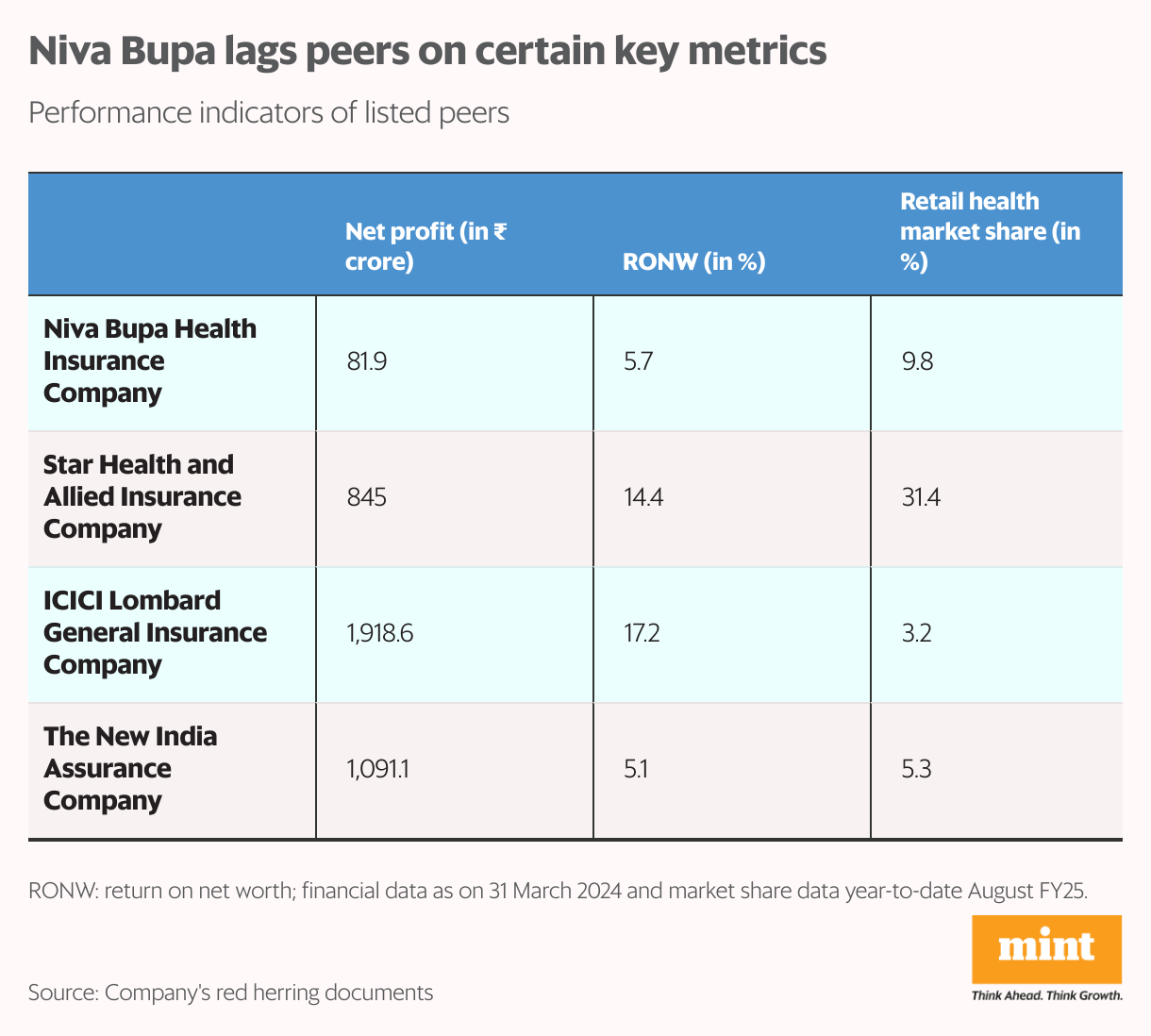

Niva Bupa faces intense competition from established players and new entrants, which could erode its market position. Lagging behind peers on key performance metrics may further hinder its growth.

As of 31 March, Niva Bupa reported a net profit of ₹81.9 crore and posted a return on net worth of 5.7%. However, competitors like Star Health, ICICI Lombard, and The New India Assurance have outperformed Niva in these metrics. Moreover, Niva Bupa’s 9.8% share of the retail health market is smaller compared to its rivals, reflecting a more limited market presence.

Bathini sees this otherwise. “While Niva Bupa’s current market share may be relatively smaller, it is important to note that India remains an underpenetrated market for health insurance.” “Despite this, Niva Bupa has demonstrated significant growth in its overall premium, with a compound annual growth rate (CAGR) of 41%,” he added.

Also read: Which way will Sensex swing in new Samvat? Inaugural Mint survey joins the dots

Mahendra also notes that the company made strategic moves to enter new segments, such as the group insurance business, which previously had minimal involvement. “As we build up from a lower base, our growth rate in this segment is faster than our overall growth. In terms of market share in retail health, we’ve seen substantial improvement from 4.2% in FY20 to 9.9% currently, demonstrating rapid expansion across all channels,” he added.

Retail health boom

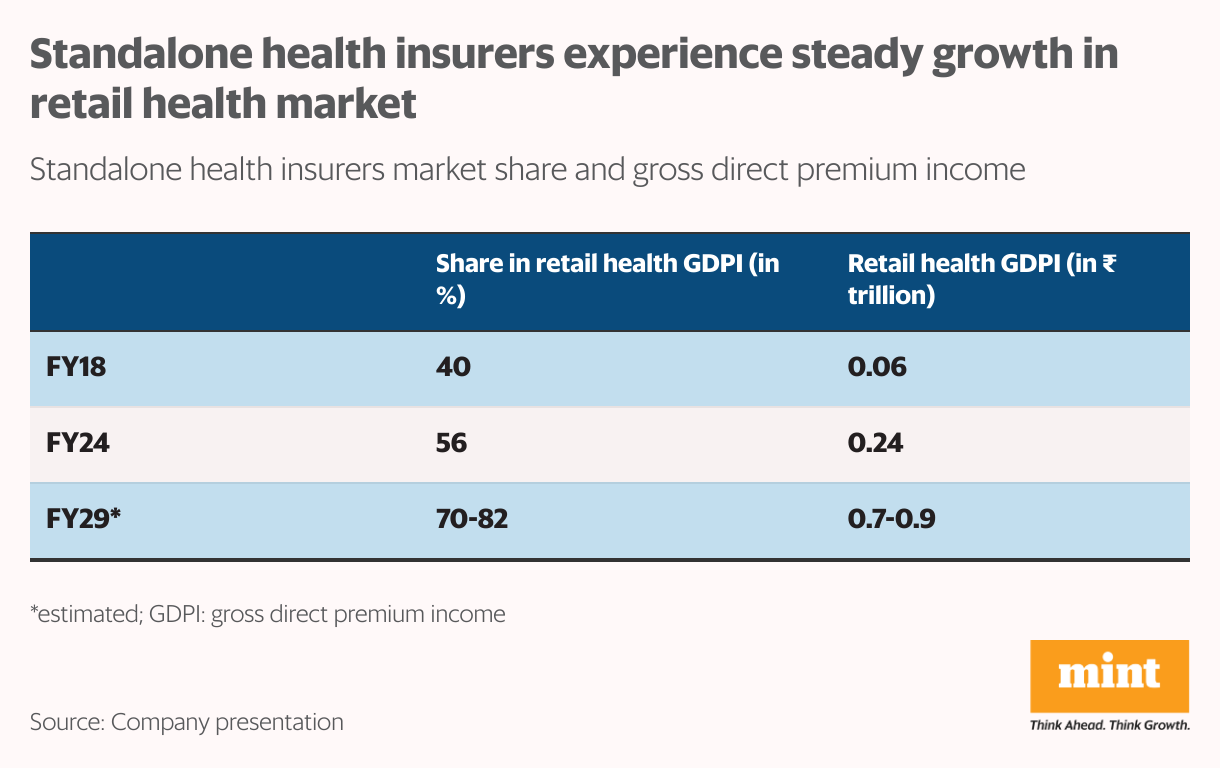

The rapidly expanding retail health insurance sector presents substantial growth potential for Niva Bupa. As a standalone health insurer, Niva is strategically positioned to capitalize on this growth and strengthen its market presence.

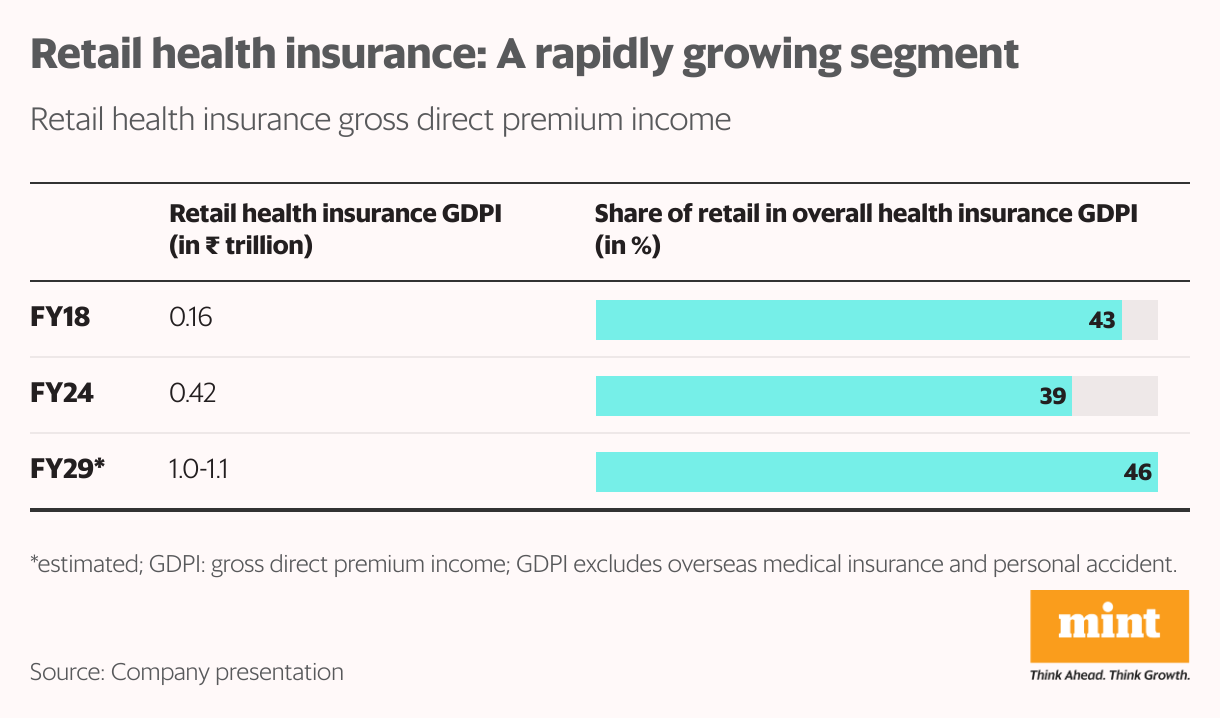

The retail health insurance market in India has emerged as a fast-growing sector. Standalone health insurers have been experiencing steady growth in the retail health insurance market. Their share of the retail health gross direct premium income (GDPI) has grown from 40% in FY18 to 56% in FY24. According to the Redseer industry report, this trend is expected to continue, with their share projected to reach 70-82% by FY29. Correspondingly, the GDPI for standalone insurers is estimated to increase from ₹0.06 trillion in FY18 to ₹0.7-0.9 trillion by FY29.

Moreover, the GDPI from retail health insurance is also expected to see a remarkable growth, rising from ₹0.16 trillion in FY18 to an estimated ₹1.0-1.1 trillion by FY29, translating into a CAGR of 18-21%. The share of retail health insurance in the overall health insurance GDPI is projected to increase from 43% in FY18 to 46% by FY29, as per the report.

Meanwhile, as the company continues to grow, it needs to ensure sufficient capital to support its expansion. The IPO proceeds will help it provide the financial stability required to fuel growth initiatives by enabling it to meet regulatory solvency requirements. “This will position us well to pursue our long-term growth strategy while managing operational risks effectively,” said Mahendra.