{kind=link}

Global IT giant Accenture’s Q1FY25 results surprised positively with constant currency (CC) revenue growth of 8% year-on-year, beating its 2-6% guidance. Growth was broad-based but led by the healthcare and public services vertical where Accenture has relatively higher exposure than tier-I Indian peers. Consulting business revenue rose 6% year-on-year in CC terms. Managed services (outsourcing)—where Accenture competes with tier-I IT companies—saw growth improve to 11%. Strong Q1 pushed Accenture, which follows a September-August financial year, to raise its FY25 CC revenue growth guidance to 4-7% from 3-6% earlier.

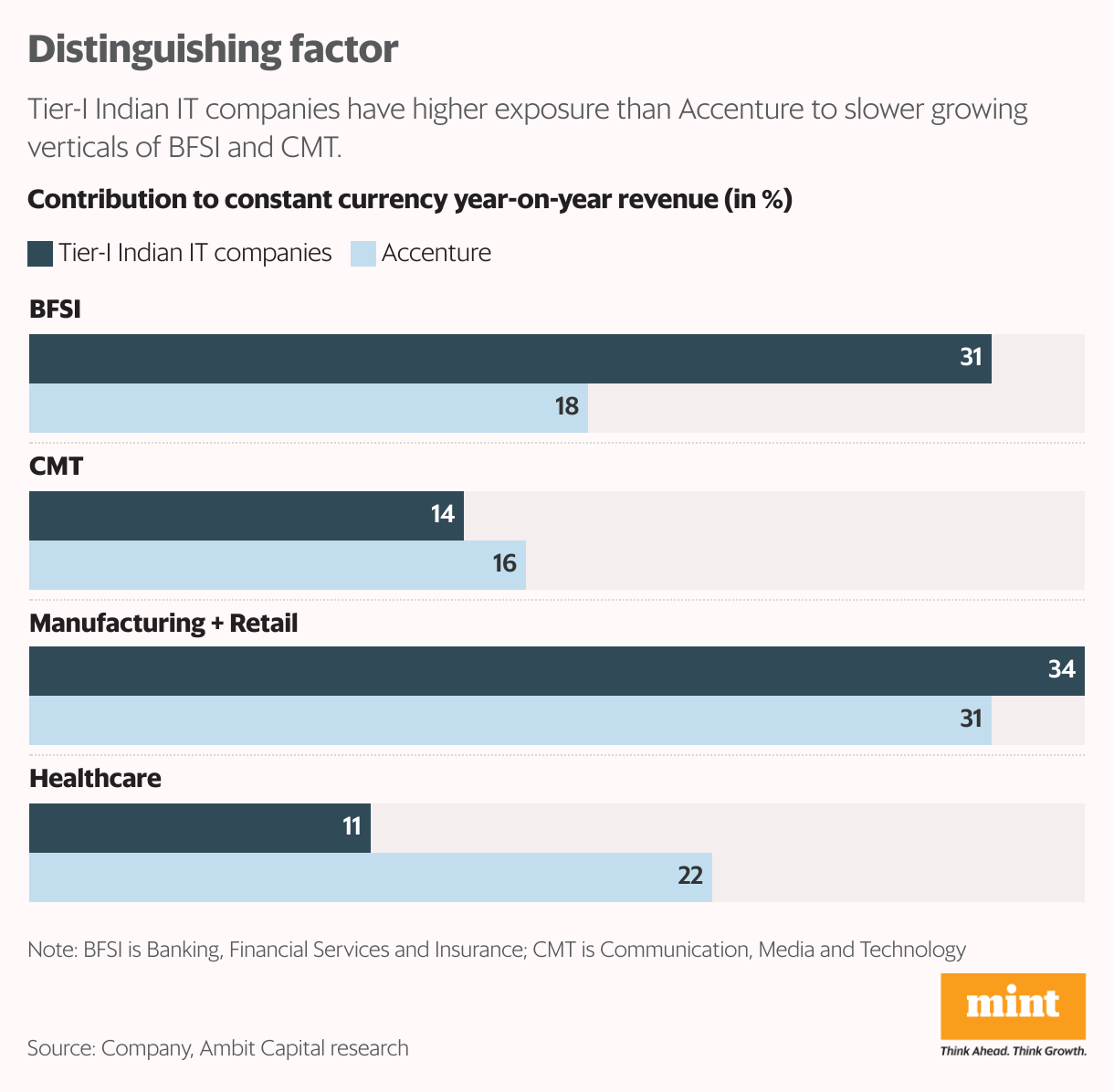

Accenture’s result is often seen as an indicator for future performance of tier-I Indian IT firms. But despite its positives, Indian IT investors’ sentiment was muted. On Friday, the Nifty IT index was down 2.63%.

The Accenture management attributed revenue growth to better execution of large deals rather than demand improvement. While the FY25 guidance has been raised, there is no material change in the discretionary demand environment for IT services. Clients continue to prioritize large transformation deals and critical programs, while smaller deals remain under pressure. In Q1FY25, Accenture’s order inflow was driven by a record 30 large deals of $100-million plus. The top end of the guidance assumes more of the same spending environment, while the lower end assumes a little more deterioration in spending in FY25 versus FY24, the management said. Clarity on clients’ budgets typically emerges only by January-February. Accenture also pointed to pricing pressure in the market, which is a negative.

Read more: With multifold gains, is GE Vernova T&D stock running ahead of its earnings?

“Accenture’s improving deal total contract value share indicates its growth, especially in Managed Services, might be coming at the expense of India IT Services peers, a negative,” said JM Financial Institutional Securities report on 19 December. Simply put, given a still constrained client budget, it might reflect potential market share loss for Indian IT companies. Further, Accenture is seeing challenges in Europe and mixed trends in financial services across regions. So, JM Financial cautions against extrapolating Accenture’s performance to that of Indian firms. In any case, the December quarter (Q3) is seasonally weak for the sector due to furloughs.

A part of the correction in Nifty IT index can also be attributed to sell-off seen in global and Indian equities reacting to a hawkish US Federal Reserve. Accenture’s Q1FY25 result released on Thursday followed by the US Fed’s 25-basis-point interest rate cut on Wednesday. While the rate cut was in-line with expectations, Fed said that it may lower rates only twice in 2025, versus a higher number of rate cuts estimated earlier. A basis point is one-hundredth of a percentage point.

The US is a crucial market for Indian IT companies and a revival in discretionary technology spending, especially by banking, financial services and insurance (BFSI) clients, would depend on macro-economic stability of the US economy. Any hiccups here would mean a slower recovery in IT spending, lowering revenue visibility. Another monitorable would be the impact of US President Donald Trump’s potential change in healthcare reforms. Since the healthcare vertical has held the fort for Indian IT companies lately, uncertainty in the US government spending would be a dampener.

Meanwhile, in FY25 so far, the Nifty IT index is up around 26%, beating the Nifty 50 index’s single-digit returns. This has been fuelled by hopes of rapid revenue recovery, pushing valuations higher. But given the mixed signals, caution is warranted. “Tier-I/tier-II IT one-year forward price-to-earnings valuations of 29.9x/45x (67%/171% premium to pre-Covid 3-year average) suggest expectations are elevated, driving our stance that pain is not over in IT,” said an Ambit Capital report on 20 December. Ambit continues to expect a modest recovery, but with growth, margins and cash generation staying below pre-covid for tier-I IT.