{kind=link}

The issue opens on Wednesday, 6 November, and closes on Friday.

As a dominant player in India’s hyperlocal commerce market, Swiggy boasts a strong brand, robust business model, and a rapidly growing user base. It offers a range of services through a unified app, allowing users to browse, order, and pay for food, groceries, household essentials, and more.

Additionally, the platform offers services such as restaurant reservations, event bookings, and on-demand pick-up and drop-off services.

Also read | Swiggy IPO set to cook up a storm for early backers, deliver up to 35x returns

Swiggy proposes to utilize the net proceeds from its IPO to expand its dark store network for quick commerce and enhance its brand awareness and visibility across segments. “We are continuing to expand our geographical presence as well as densifying our store network in the larger metros,” said Rahul Bothra, chief financial officer at Swiggy, in an interview with Mint.

This will also improve logistics and cost efficiency, he added.

Mukul Goyal, co-founder of Stratefix Consulting, said key investment areas from the IPO proceeds would include technology enhancements for demand forecasting and route optimization, which could lower delivery times and reduce fuel expenses.

A hyperlocal commerce powerhouse

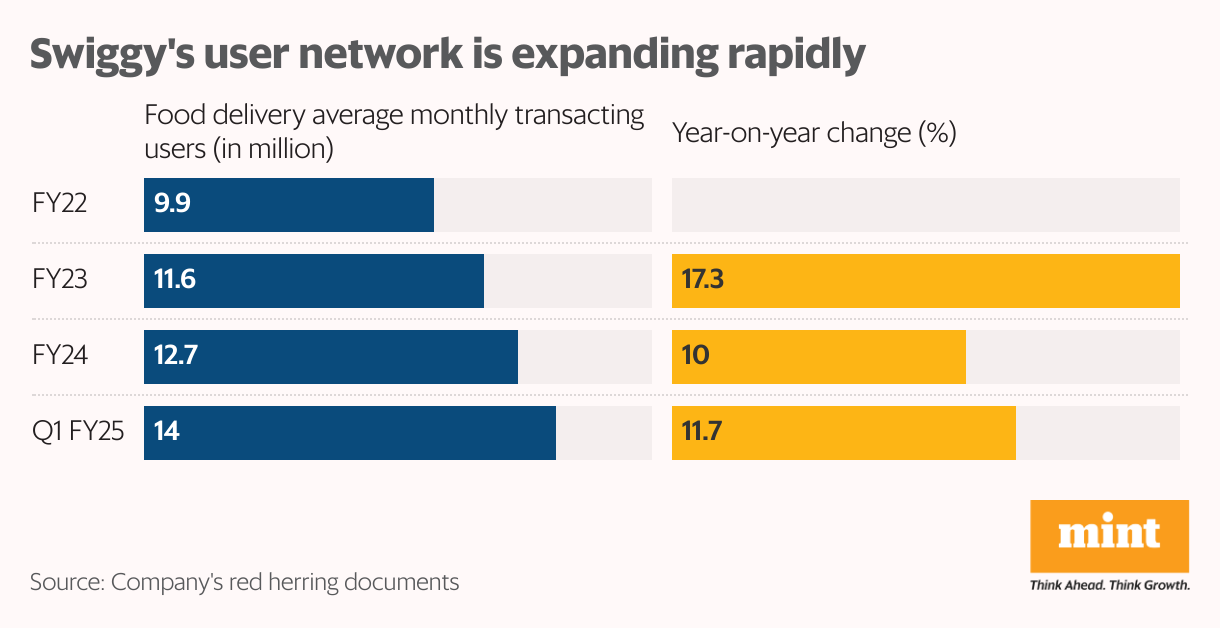

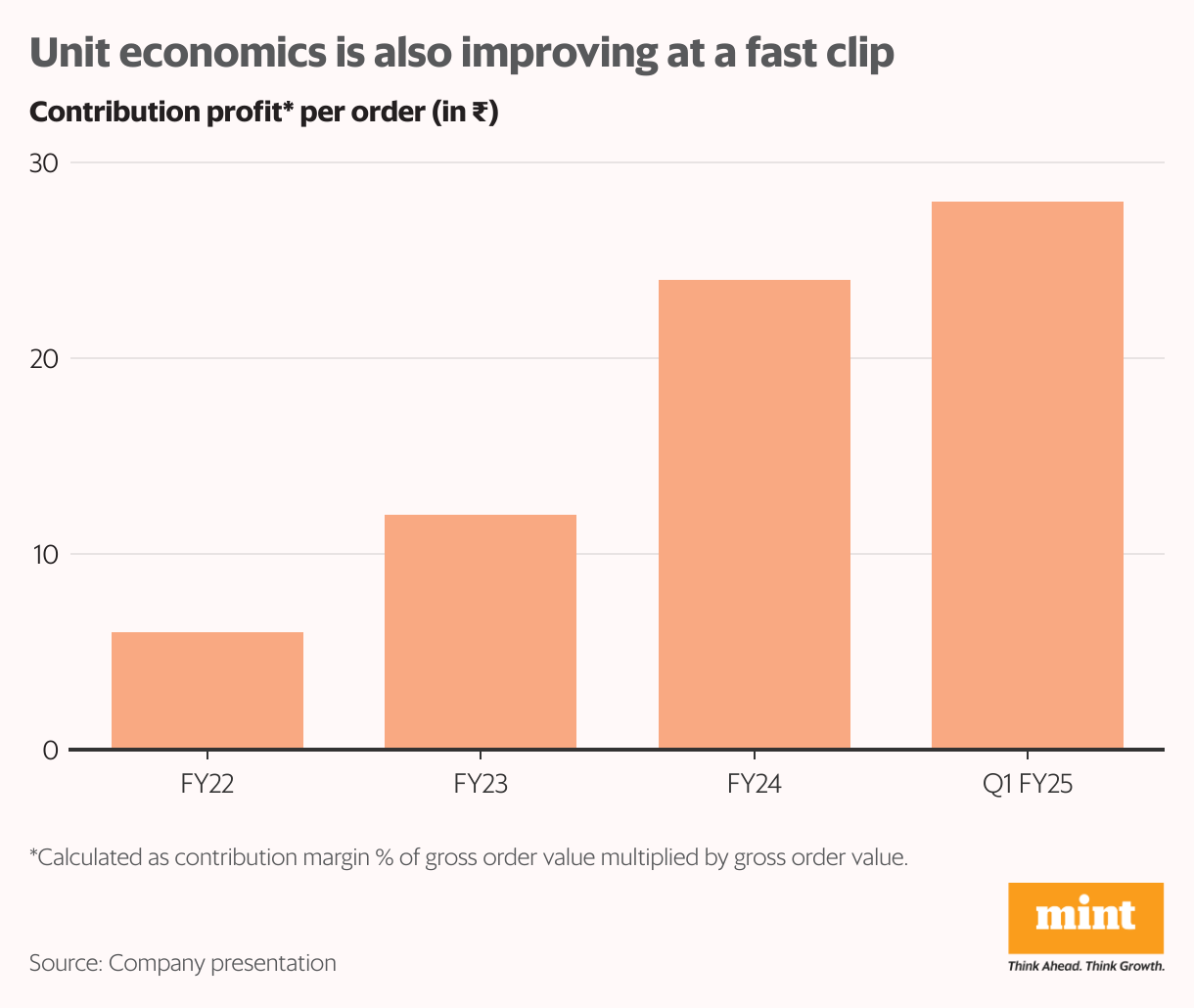

Swiggy has solidified its position as a dominant player in India’s hyperlocal commerce landscape. Its monthly transacting user base has expanded significantly by 28.3% over the previous three fiscal years. This, and a quadrupling of its contribution profit per order over that period, has significantly improved Swiggy’s financial performance.

Despite the high costs of quick commerce, Swiggy has sustained a broad geographical reach in the previous three years. Further, its unified app for offering multiple services boosts convenience and accessibility.

“Swiggy’s approach of an integrated app offering versus Zomato’s multi-app approach (both at the back- and the front-end) helps it innovate faster (Instamart was born out of a similar synergy),” Motilal Oswal said in a report. “Swiggy could again be at the forefront of food delivery innovation through Bolt, its 10-minute food delivery platform,” it said.

Also read | Capital is not going to decide winners in quick commerce: Swiggy’s Sriharsha Majety

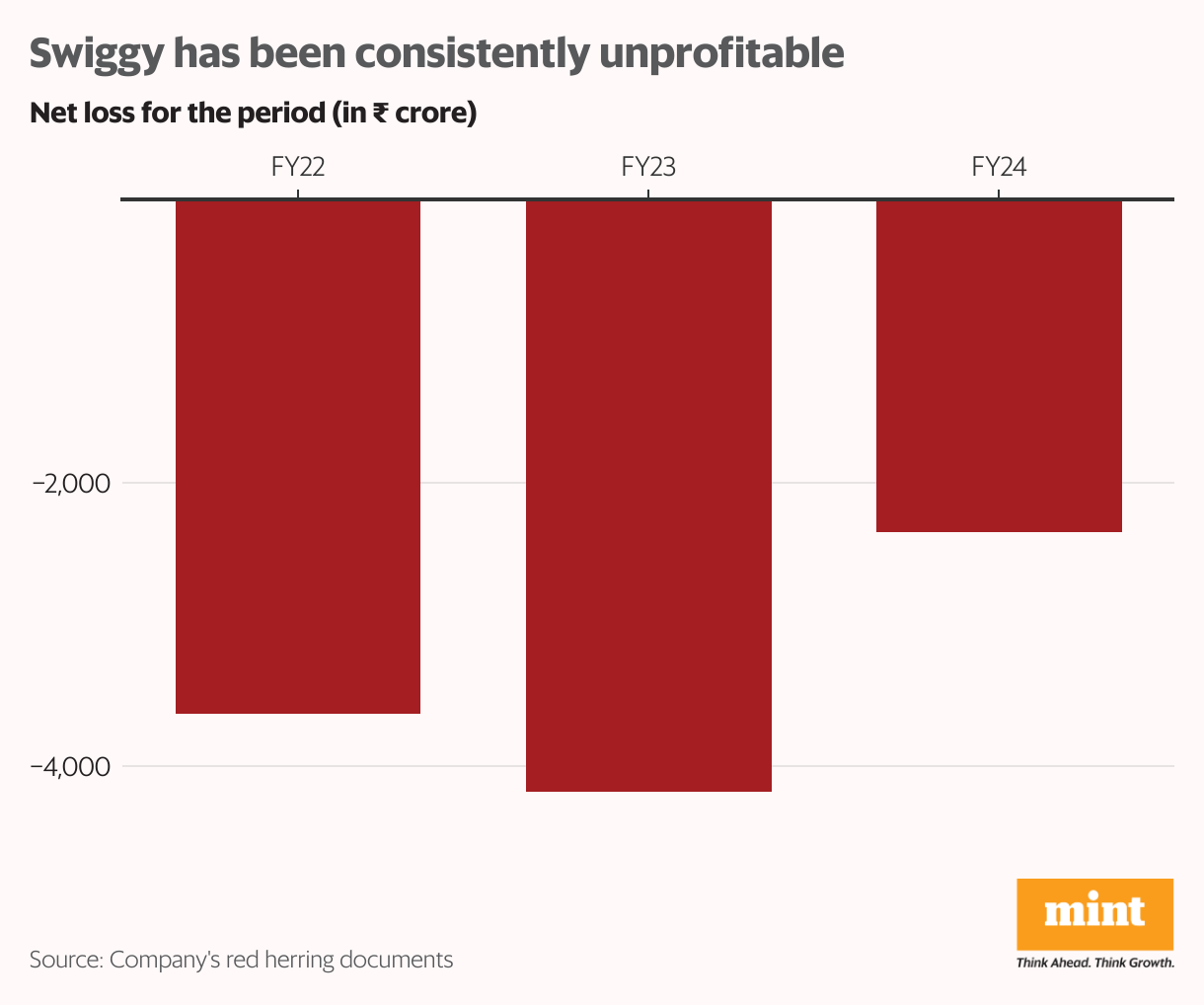

Persistent losses

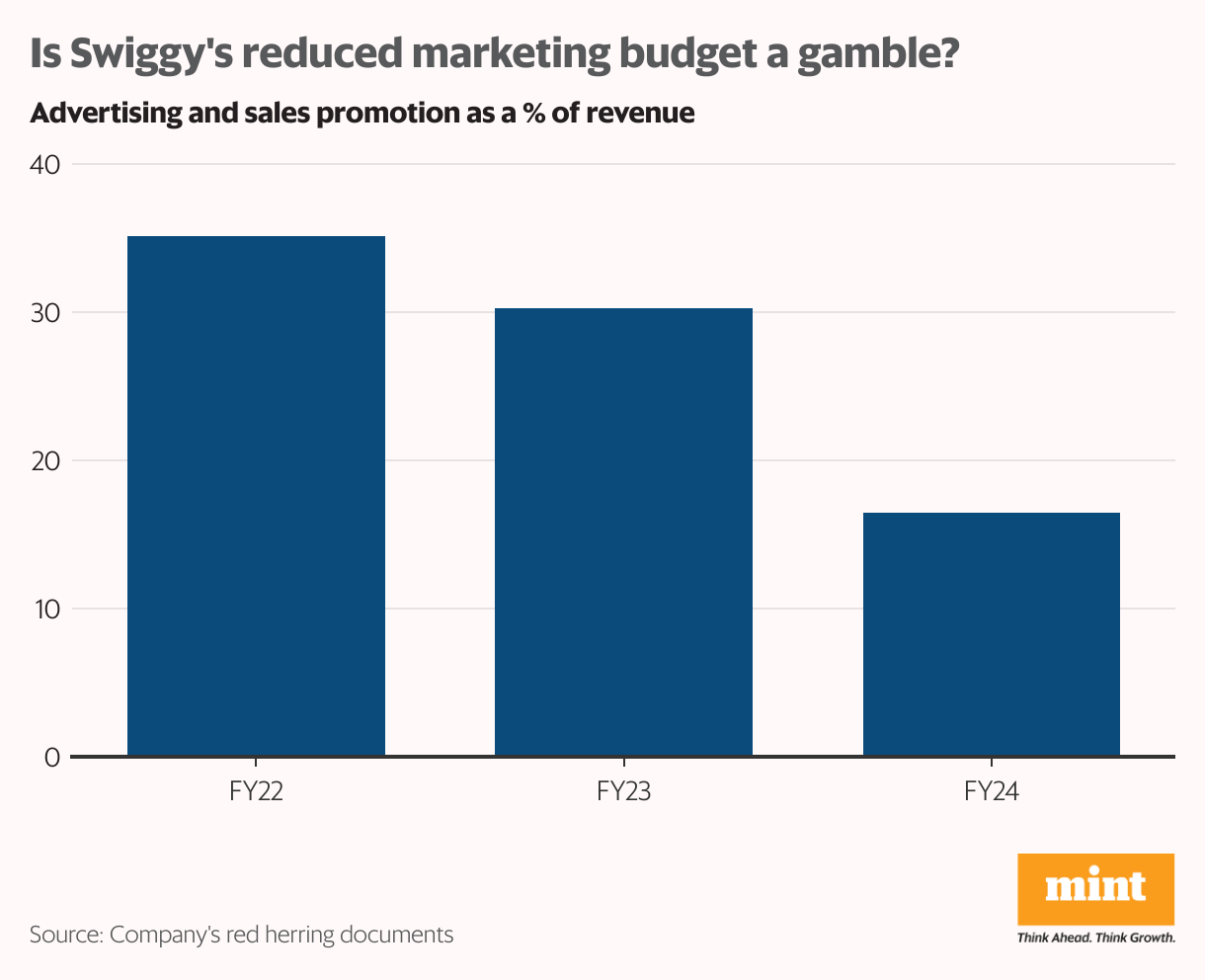

Swiggy has significantly cut its marketing expenditure, from 35.2% of its revenue in 2021-22 to 16.5% in FY24. “As India’s leading consumer technology platform, Swiggy enjoys strong brand recognition, which allows it to attract a substantial number of customers organically. This decreased reliance on performance and affiliate marketing has led to lower customer acquisition costs,” Bothra said.

Is Swiggy’s reduced marketing budget a gamble? Analysts remain divided.

“Swiggy’s advertising and promotion costs remain above the industry average, even after a 26% cut in FY24. This reduction hasn’t impacted the core food delivery business, which grew by 27% in FY24, up from 22% in FY23,” said Christy Joseph, research analyst at Geojit Financial Services.

“However, the quick commerce segment, being highly competitive and relatively new, requires more advertising to gain market traction,” he added. “Swiggy’s Instamart is behind its peers in overall growth and average store revenue, mainly due to fewer store additions and lower marketing expenses. Despite this, the company remains focused on reducing its promotional expenses in the long term,” Joseph said.

“The company has been focusing on selective advertising during events like festivals and sports seasons, where consumer activity is high. This targeting helps in maximizing reach by connecting with consumers during peak engagement times,” said the research team at Master Capital Service.

Despite its brand strength, Swiggy reported a staggering loss of ₹2,350 crore for FY24. The logistics segment has been particularly challenging for it.

“While our Indian subsidiary Scootsy Logistics has encountered rising losses, we are implementing strategies to address these issues,” Bothra said. “Our acquisition of LYNK Logistics last year enhances our distribution network, enabling efficient delivery of FMCG products to kirana stores and traditional retailers. We expect both Scootsy and LYNK Logistics to benefit from scale and operational efficiencies, leading to improved profitability.”

Additionally, Zomato held a slight edge over Swiggy in the dark store race, operating 526 active dark stores compared to Swiggy’s 523 in FY24.

Swiggy aims to expand its geographic presence and increase the density of its dark store network in major metropolitan areas. “The number of dark stores is expected to grow significantly, with plans to increase the average store size from 3,000 sq.ft. to 4,000 sq.ft,” Bothra said.

Swiggy aims to expand its dark store presence in both its existing and new markets. “The strategy involves not only opening new stores but also increasing the density of stores in high-demand areas to ensure rapid delivery,” said the research team at Master Capital Service. “To improve efficiency, Swiggy will tailor its dark store sizes and layouts according to the requirement in each locality.”

Also read | How dining and events could be Swiggy’s next growth engine

Fight for survival

A competitive landscape, however, poses significant challenges to Swiggy’s growth and profitability. Despite its dominant market position, Swiggy’s rise in the food delivery market is increasingly challenged by Zomato’s aggressive expansion and offerings.

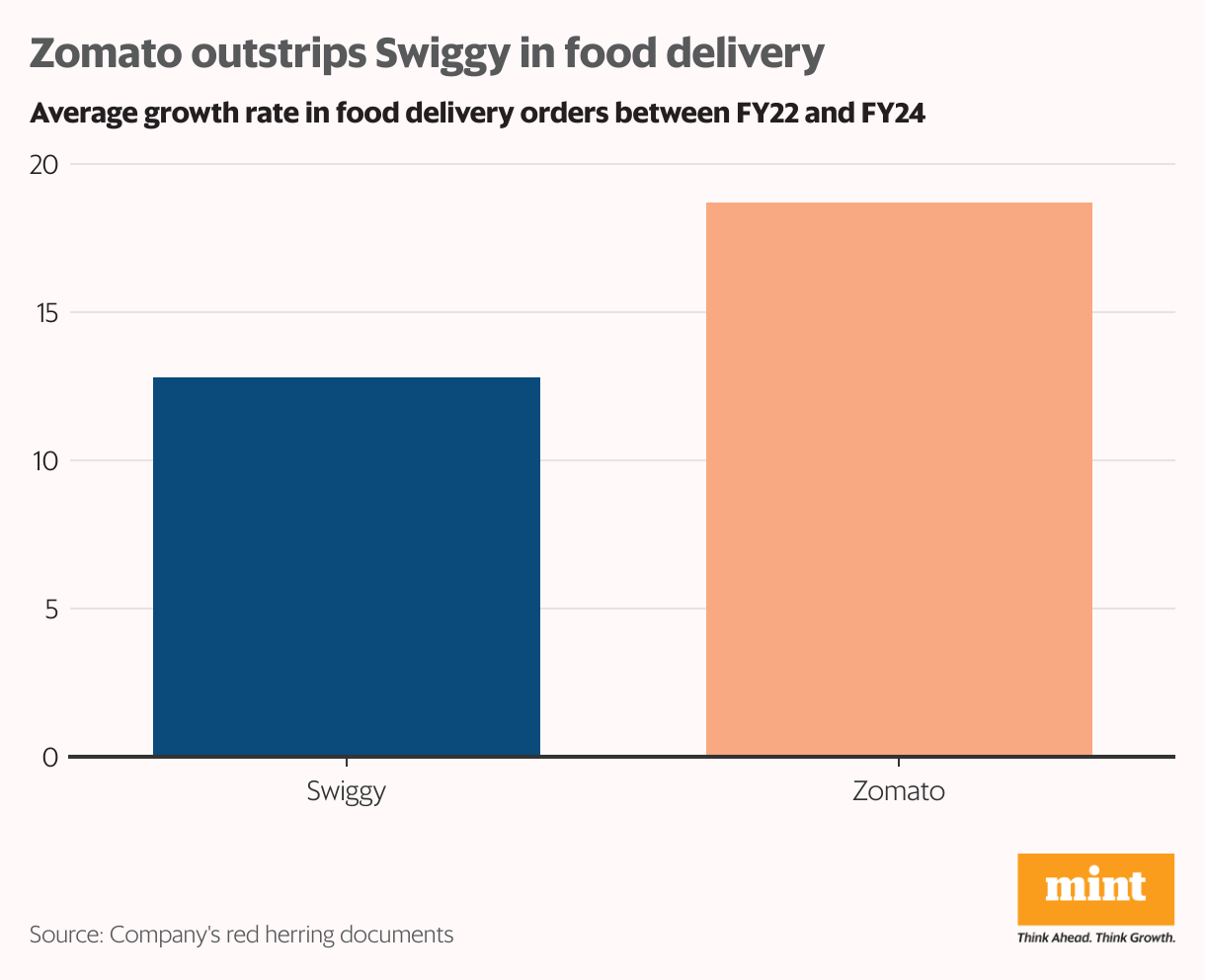

While Swiggy has carved out a substantial share in food delivery, Zomato is rapidly gaining ground. With a compound annual growth rate (CAGR) of 18.6% in food delivery orders between FY22 and FY24, Zomato has outpaced Swiggy’s growth of 12.7%, posing a challenge for Swiggy’s market share growth.

“The company plans to increase marketing investments in the quick commerce business, which is still in its early stages,” added Bothra. “As this business grows, marketing efforts will be scaled up to acquire and retain customers. Despite this, the company will maintain a focus on optimizing marketing spend to maximize returns.”

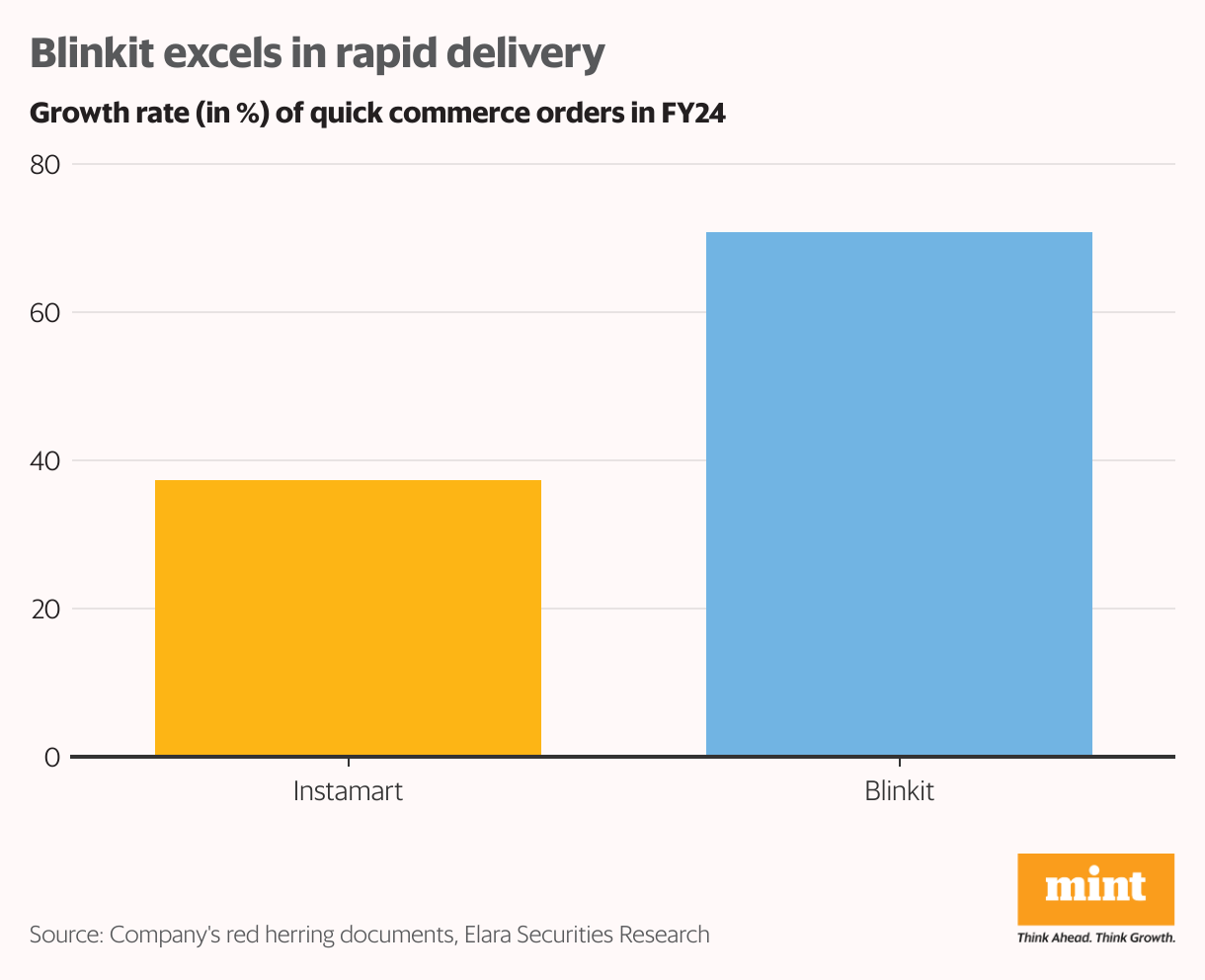

Instamart was initially a frontrunner in the quick-commerce arena but Zomato-owned Blinkit has recently overtaken it with year-on-year growth of 71% in orders in FY24, compared to Instamart’s 37.4% growth.

Additionally, Zepto is emerging as a formidable competitor with its aggressive strategies and swift expansion.

However, Swiggy’s cohorts appear more mature and stickier in terms of gross order value per user even as Zomato has gained share in food delivery, Motilal Oswal said in its report. “In quick commerce, Blinkit and Zepto have made strides, but Swiggy can still differentiate itself through a broader selection and customized SKU strategy,” it added.

Also read | Swiggy’s quick commerce bet faces tough crowd as IPO nears

The online food delivery wave

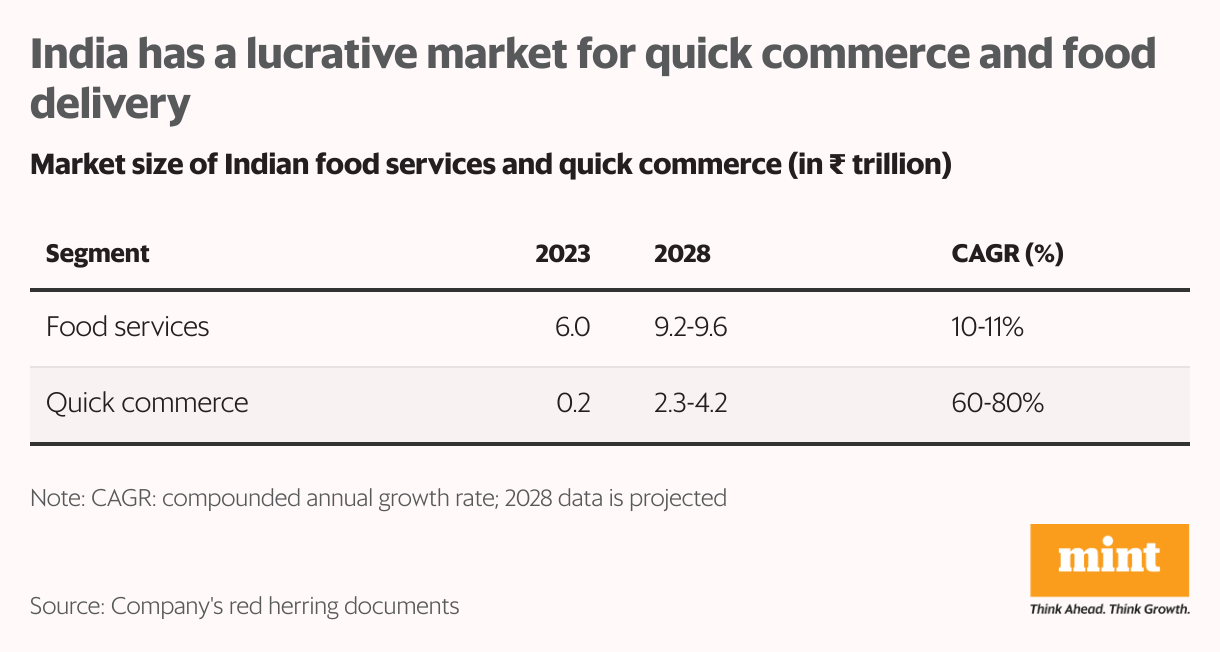

The Indian market presents a wealth of lucrative opportunities for e-commerce and food delivery, particularly due to its under-penetrated nature compared to global economies, which indicates substantial growth potential.

Within this landscape, different segments are poised for significant expansion. The food services sector is expected to experience steady growth as online food ordering and delivery become increasingly popular among consumers.

Retail is also on an upward trajectory, driven by the rise of e-commerce and organized retail, which is transforming shopping habits.

The most exciting potential lies in the quick commerce segment, which is projected to grow explosively at a CAGR of 60-80%. As consumers increasingly seek the convenience of rapid delivery for groceries and essential items, this segment is set to become a cornerstone of the evolving marketplace, making it an opportune moment for businesses to capitalize on these trends.

“Swiggy aims to provide innovative solutions for urban users, targeting significant growth in the online food delivery and quick commerce markets, which is projected to grow at 17-22% and 60-80% CAGR, respectively, between 2023 and 2028,” said Deven Choksey, managing director of KRChoksey Financial Services.

Also read | Swiggy IPO: How investors justify risky pre-listing trading