{kind=link}

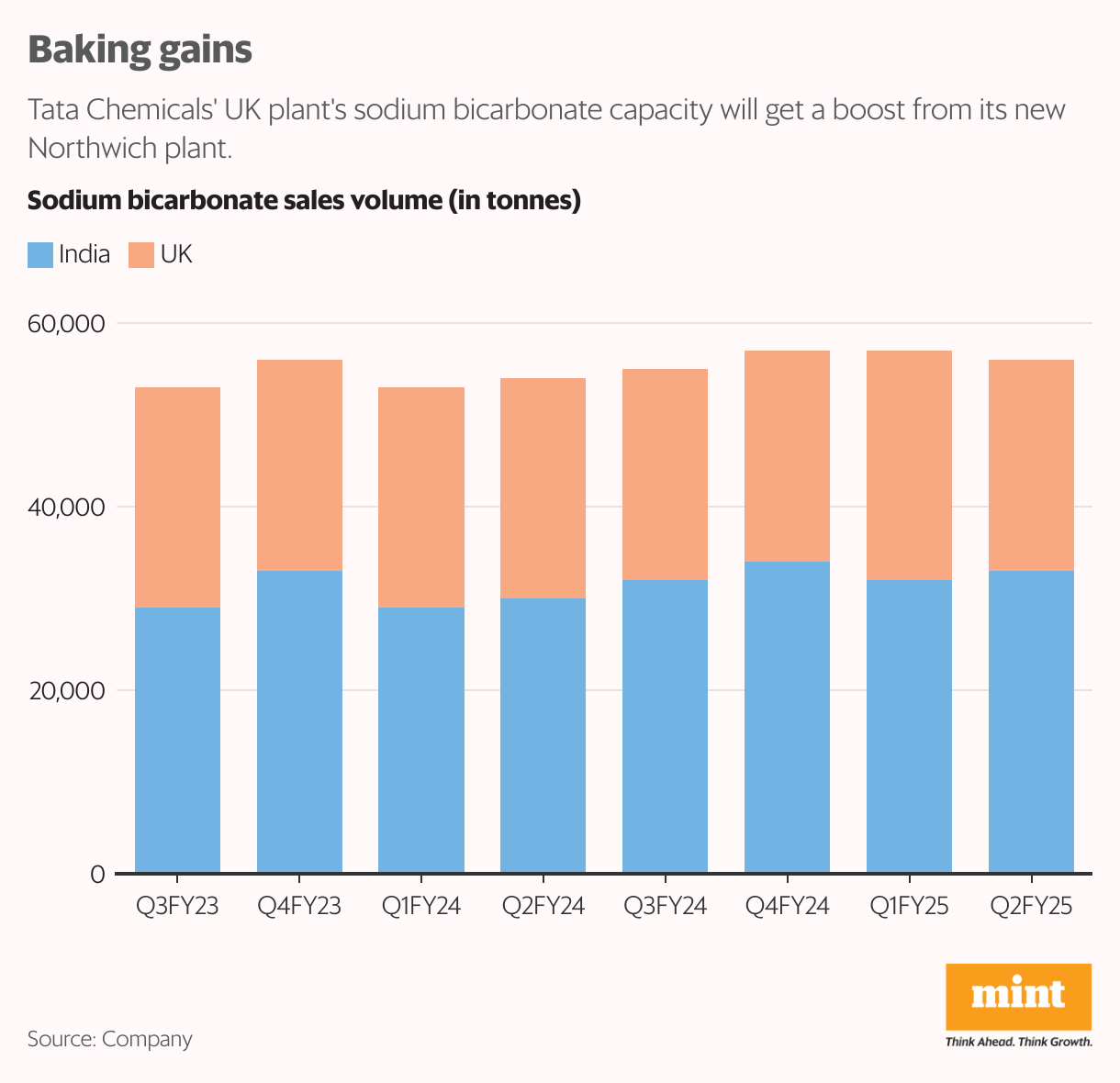

Tata Chemicals Europe Ltd (TCEL), a subsidiary of Tata Chemicals Ltd, has embarked on a restructuring exercise. This involves shutting down its Lostock soda ash manufacturing facility by January and setting up a new plant in 2025 to manufacture value-added pharmaceutical-grade sodium bicarbonate (VAPSB) in Northwich.

Recall that an impairment charge of ₹963 crore mainly related to the Lostock plant drove the whopping 82% year-on-year drop in Tata Chemicals’ consolidated FY24 reported net profit to ₹449 crore. TCEL’s volume at about 6 lakh tonnes formed about 30% of total FY24 consolidated volumes. However, Ebitda contribution is much lower at 12% of FY24 consolidated Ebitda of ₹2847 crore.

After the restructuring, TCEL’s volume will stay unchanged broadly, as the Lostock plant’s soda ash capacity of about 2 lakh tonnes will be offset by 1.8 lakh tonnes of the Northwich VAPSB plant by 2027. What’s crucial is that the Northwich plant’s Ebitda margin is likely to be higher due to the value-added nature of the product.

Tata Chemicals will incur a capex of ₹655 crore to set up the new plant. While the new VAPSB plant will be commissioned in about three years, there could be some indication of profitability by Q3FY25. That’s because a manufacturing capacity of about 90,000 tonnes in the UK for the same product was commissioned in October. The first output will be delivered initially to non-pharma customers till the company is qualified by customers from the pharma industry during Q3FY25.

Even so, the immediate boost to consolidated volume could come from the 1.85 lakh tonnes of additional soda ash capacity in India that was completed in September. Tata Chemicals expects volumes of the Indian operations to rise in Q3FY25.

Also Read :Tata Steel investors may remain jittery amid delayed revival in European operations

To be sure, over the past couple of years, Tata Chemicals’ shares have mostly been rangebound as it largely remains a play on soda ash cycle. There have been intermittent spurts mainly due to rumours of the listing of Tata Sons where Tata Chemicals has a 3% stake.

The stock now trades at a price-to-earnings multiple of 24x and EV/Ebitda 11x, based on Bloomberg consensus estimates for FY26. The stock seems to be fairly priced amid the current dynamics in the soda ash market.

According to chemanalyst.com, the Asian soda ash market continues to face downward pressure in early November, with persistently high production output and limited downstream demand. Soda ash producers have maintained elevated output levels, contributing to extremely high inventory levels.

Also Read: Ratan Tata made India a better, kinder place