{kind=link}

Gold is the ultimate contrarian asset. It hedges against inflation, protects from risk and has a low correlation with equity. Yet, last month, gold prices surged to an all-time high of $2,530 per troy ounce, defying expectations amid declining inflation and strong equity markets. This unusual rally reflects the complex mix of factors driving gold demand. Since gold doesn’t pay coupons or dividends, the opportunity cost of holding it plays a critical role in returns, primarily influenced by shifts in interest and exchange rates.

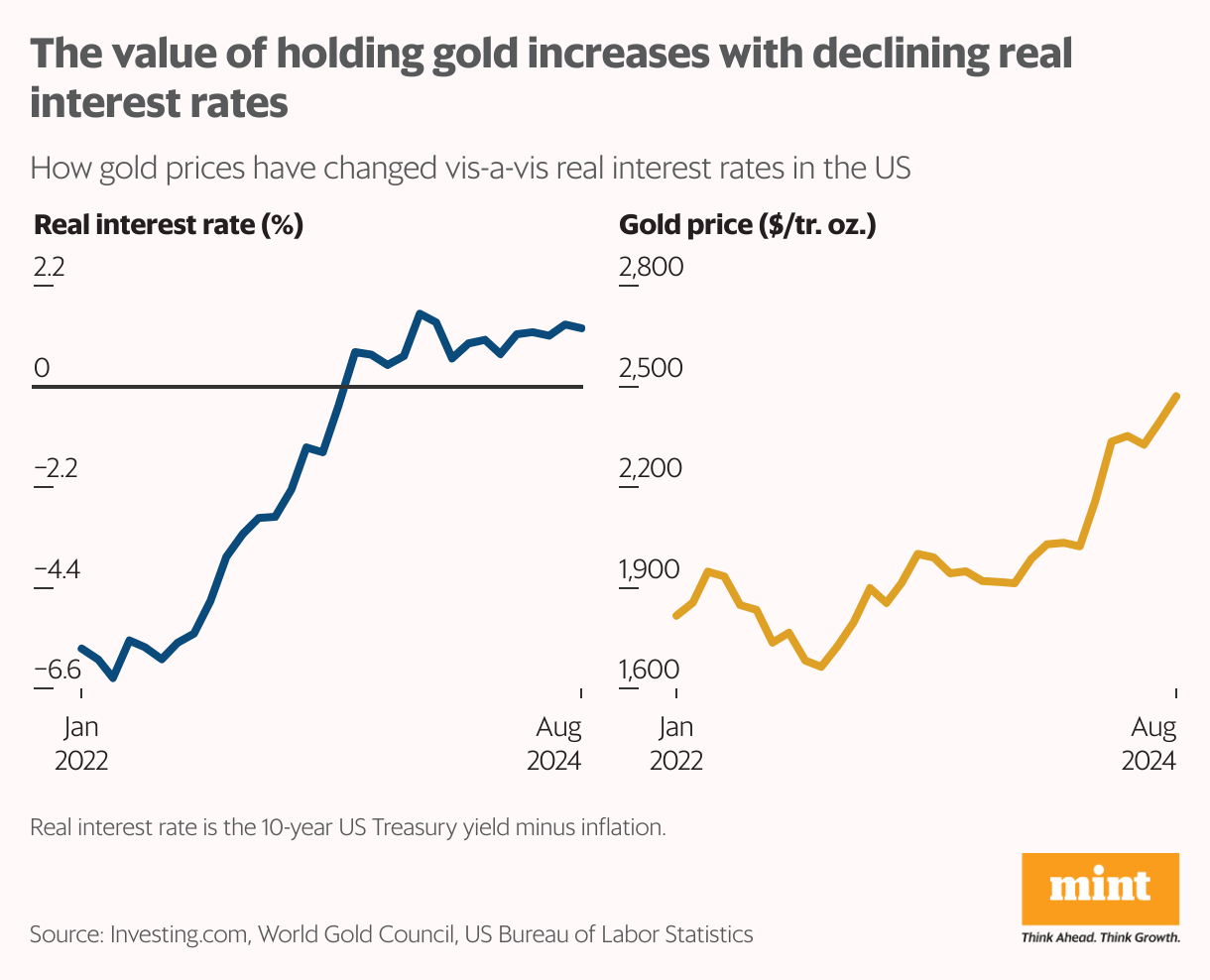

A rise in real interest rates (i.e. interest rates minus inflation) diminishes gold’s appeal: from a yield perspective, investors are better off holding treasury bonds rather than a non-yielding asset like gold.

Read this | Are sovereign gold bonds the new ‘gold standard’ in investing?

In recent months, however, US bond yields have declined, driven by expectations of easing monetary policy, and they’ve fallen more than inflation. From January to August, the two-year treasury yield dropped by 33 basis points (bps), and the 10-year yield fell 24 bps, while inflation decreased by 20 bps between January and July. This compression in real yields has provided bullish momentum for gold.

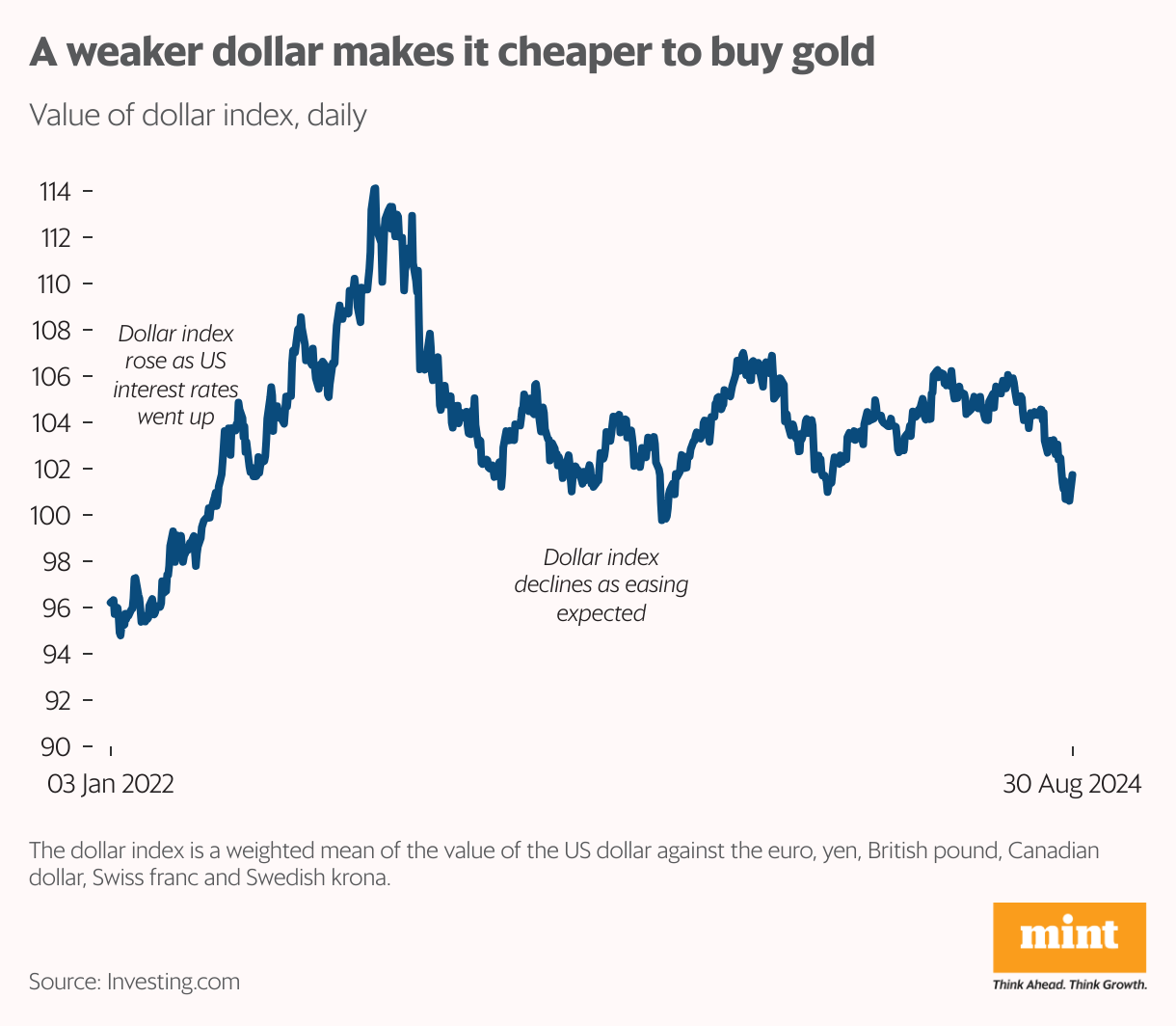

The anticipation of monetary policy has also weakened the US dollar. Since gold is priced in dollars, a weaker US greenback makes it cheaper for investors with other currencies to buy gold. The dollar index dropped by 2.3% in August alone, following a signal from Fed Chair Jerome Powell about potential easing in September—adding a modest, but noticeable, lift to gold demand.

The China factor

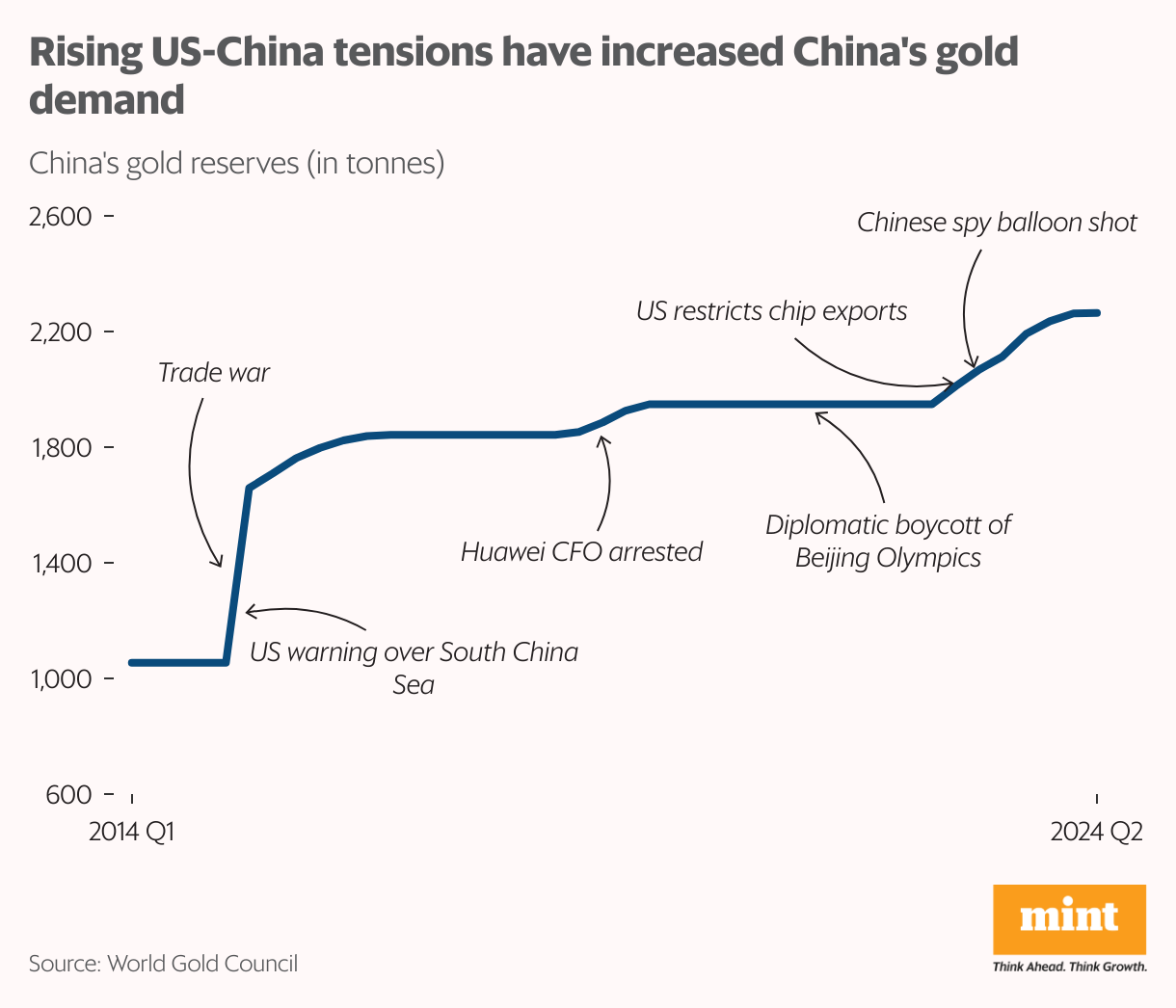

Chinese demand, both institutional and individual, is another critical driver of global gold demand. The People’s Bank of China began significantly increasing its gold reserves around 2015, in response to rising US-China tensions, particularly over the militarization of the South China Sea. Each escalation in US-China friction has pushed Beijing further towards de-dollarizing its reserves. By the end of July 2024, China’s central bank held 2,264 tonnes of gold, making up 4.9% of its total reserves.

More here | Central banks are betting big on gold. Here’s how to profit from the trend

On the consumer side, individual demand for gold in China, including jewellery and investment products like bars and coins, rose by 15% in 2023. This surge was fuelled by concerns over a potential renminbi devaluation, a weakening real estate market, and slowing economic growth. With uncertainties continuing into 2024, particularly as a new US president may take office later this year, China remains cautious. Some in the country view the US presidential candidates as “two bowls of poison”—one unpredictable, the other unknown.

Debased currencies

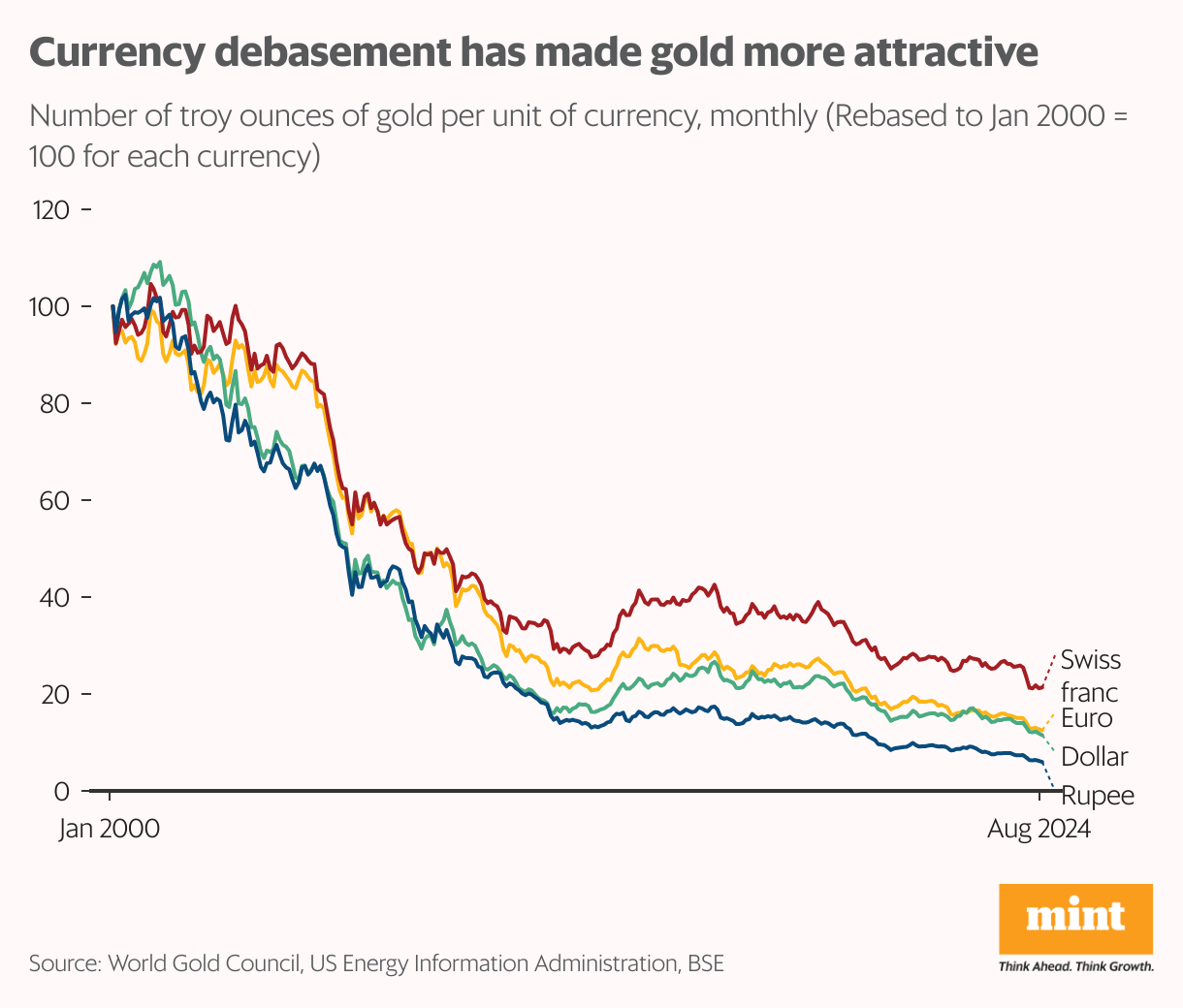

The increase in money supply in advanced economies, which started with quantitative easing, continued via fiscal support during the pandemic, and culminated in high inflation and rising sovereign debt. Collectively, this has led to a loss of value in fiat currencies. Flipping the unit of measurement to gold shows the extent of currency debasement. In terms of gold, the dollar’s value in August 2024 was merely 11.5% of its value in January 2000; the Swiss franc was marginally better at 21.3%.

And this | Sinking copper-gold ratio signals elevated global economic distress

Gold has held strong against physical and financial assets, too. An ounce of gold was worth 30 barrels of Brent crude in August 2024, up from 11 barrels in January 2000. The Sensex-to-gold-price ratio dropped sharply in August, after declining through 2024. Greater awareness of the role of gold as a store of value has increased gold demand and the price that investors are willing to pay for it.

If not gold, what?

While the polycrisis of 2022 may be in the rearview mirror, geopolitical tensions persist across key regions. Conflict in West Asia poses an upside risk to oil prices, China-Taiwan tensions and maritime disputes in East Asia remain unresolved, and Europe continues to grapple with the effects of the Ukraine war on trade, defence, and politics. The resurgence of Mpox also reminded the world of the looming risk of new pandemics.

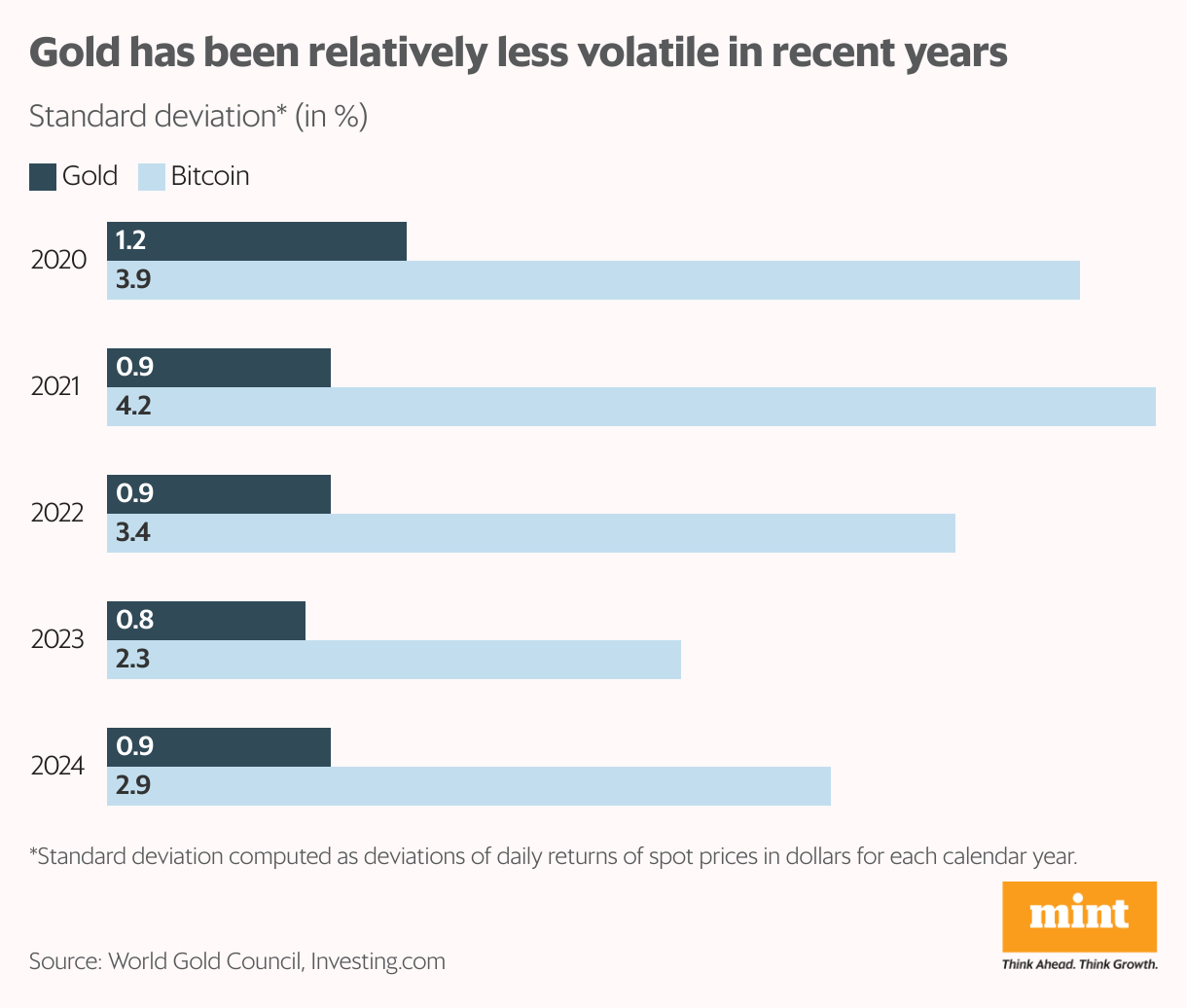

In the past, the US dollar was the sole refuge from uncertainty. But the desire to diversify reserves beyond dollars has created a need for other safe havens. There is currently no alternative to gold: non-dollar currencies are not backed by sufficiently deep and liquid markets, and bitcoin is a volatile and unproven asset. Gold continues to glitter in dark times, and each rush to gold is proof of jittery markets, fragile growth, and a risk-pocked world.

The author is an independent writer in economics and finance.