{kind=link}

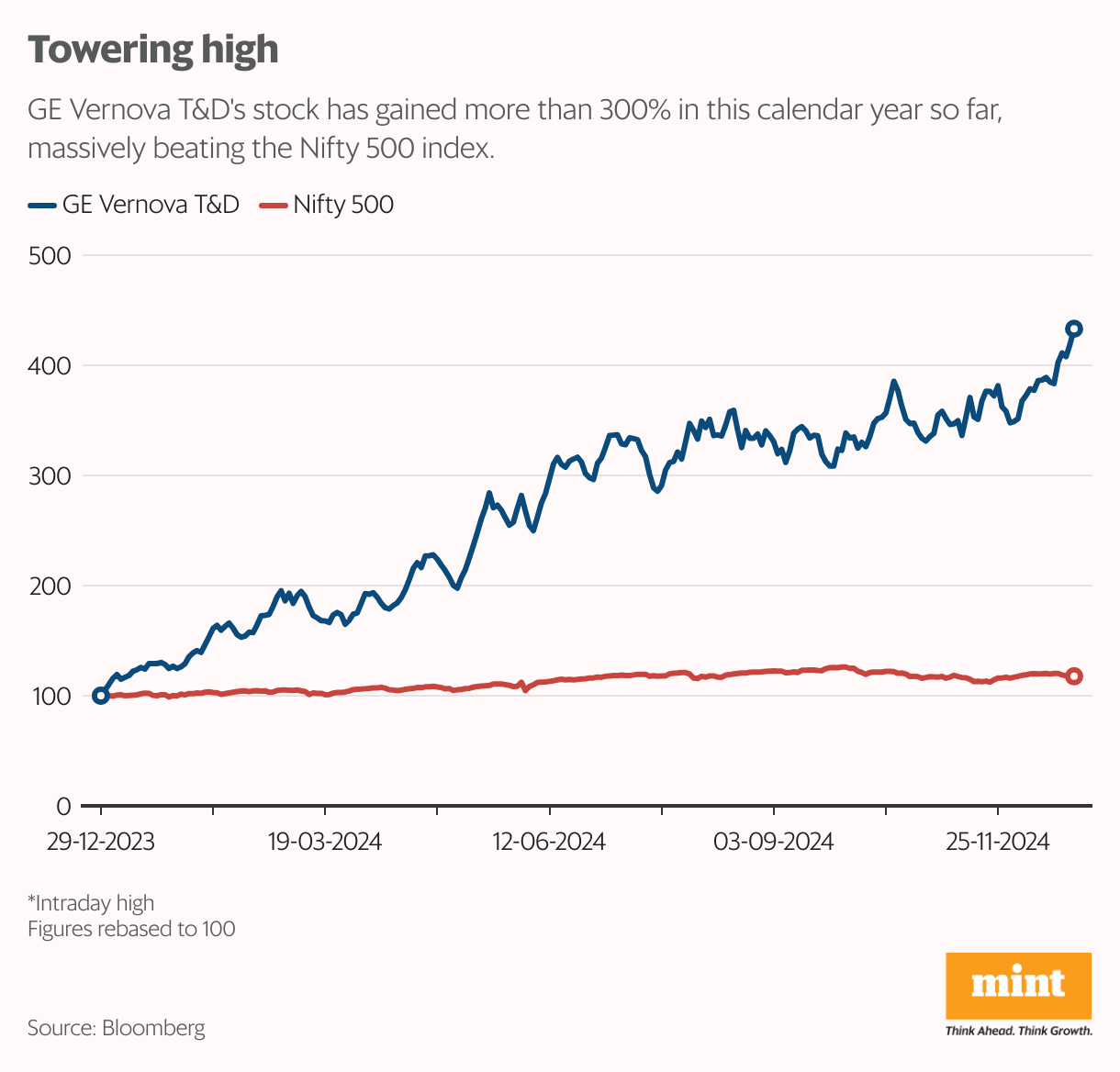

The stock of power transmission and distribution company GE Vernova T&D India Ltd is on fire. Soaring to a new 52-week high of ₹2,180 on Friday, the calendar year-to-date returns are now at a massive 330%.

On Thursday, the company bagged an order worth over ₹400 crore from Sterlite Grid 32 Ltd. for the supply and supervision of high-voltage equipment for a tariff-based competitive-bidding project. Earlier this month, it also secured an order worth around ₹400 crore from Sterlite Power for the supply of power transformers and reactors. The company will supply and supervise 765-kilovolt power transformers and reactors for Khavda.

Inflow of new orders is favourable as it aids ordering momentum and boosts the firm’s revenue visibility. Also, its parent company is outsourcing a part of the job to Indian entity. In the September quarter (Q2FY25), it received nearly ₹2,500 crore of orders from its parent, almost tenfold increase on year-on-year basis. As a result, total order inflow during the quarter rose to ₹4,700 crore, more than three times the average orders received over the previous four quarters.

The commentary is upbeat. The company expects about ₹6,000 crore of annual order inflow, excluding the large HVDC projects. Order backlog for the company stood at nearly ₹10,000 crore at the end of Q2, up 57% over end-FY24 and 2.6x trailing twelve months’ revenue. Export orders are margin accretive with better profitability for several product lines, management said during the earnings call. Exports now account for 40% of orderbook, up from 20% a year ago.

While these large projects are currently under the process of bidding, they remain prone to delays. Impressive performance in Q2FY25 with Ebitda at ₹2,000 crore, up 238% year-on-year exceeded Bloomberg consensus estimate. This led to sharp re-rating in earnings estimates by brokerages. “We raise our execution estimates by 3%/4%/6% for FY25F/FY26F/FY27F to account for robust order inflows and strong beat in 2Q. We estimate an earnings CAGR of 78% over FY24-27F,” said a Nomura Global Markets Research result review report.

Even so, its expensive valuation suggests that the stock may be running ahead of its earnings, trading at 76 times the estimated earnings for FY26, as per Bloomberg data.

Interestingly, the sale of stake by the promoter group in two tranches in the last four months, reducing its total holding to 51% from 75%, doesn’t seem to have dampened investors sentiments.

“We need to be watchful of fresh orders momentum ( ₹5,500-6,000 crore per annum is the normalised business run-rate over next two-three years) coupled with sustainability/ramp-up of OPMs (operating profit margins) levels which remain key triggers for the stock from here on,” according to Nuvama Research report.

The company remains vulnerable to risk of raw material prices volatility. Its raw material/sales ratio stood at about 60% in Q2FY25, lower end of 60-75% band recorded over the last ten quarters. Metal prices are currently under pressure because of high imports, and the imposition of a ‘safeguard duty’, under the government’s consideration, can significantly impact domestic prices.

Also Read: Use power tariffs for a transformation: The strategy Delhi needs to resolve its waste crisis